Mainstream and Critical Analyses of the Eurozone Crisis

For several years after the outbreak of the Eurozone crisis the dominant narrative blamed peripheral ‘profligacy’ and ‘inefficiency’ in running the economy and the state. The benchmark was putative German parsimony, hard work and efficiency. This perception, which became thoroughly entrenched in German policy making, drove the bailout programmes as well as the spread of austerity across much of Europe. Apparently, the rest of Europe had to go through a tough period of adjustment, following which there would be growth and prosperity.

A few contrary voices in 2010 – and some before that – did point to the extraordinary wage restraint that has prevailed in Germany since the end of the 1990s as the true cause of the profound imbalances in the European Monetary Union. These voices typically came from the critical margins of economics, and during the initial period were ignored while the Berlin narrative held sway. Gradually, as the imbalances in the Eurozone persisted, mainstream economists were also alerted to the issue. During the last two or three years it has become commonplace to identify German wage restraint as a prime cause of EMU failure.

The analytical prominence gained by German wage restraint has, however, made some heterodox, or critical, economists distinctly uncomfortable. For it could be thought that it laid the blame for the crisis on labor remuneration in the periphery, thus implicitly supporting the drive for wage restraint across the Eurozone, as promoted by Berlin and the IMF. By this token, a “genuine” non-mainstream approach would somehow demonstrate that the crisis was unrelated to labor. And what better culprit than “reckless finance”?

This is where Servaas Storm’s recent contributions come in, leading to a debate, much of it occurring on the website of INET. [1] It is not easy to present Storm’s argument in a consistent way, but he appears to claim that the Eurozone crisis was caused by the monetary policy of the ECB introducing low interest rates across the EMU and thus encouraging capital flows from the core (mostly Germany and France) to the periphery (typically Spain, Portugal, Greece). Credit bubbles ensued in the receiving countries. Meanwhile, productivity growth was exceptionally strong in Germany encouraging advanced and complex manufacturing, thus raising exports, while the periphery sunk into low-productivity, low-export, credit-driven mediocrity. The connection between credit bubbles and low productivity growth in the periphery is not clear in Storm’s analysis, but the bubbles seem to have exacerbated the skew in the productive structure of the Eurozone entirely in favor of Germany. This is, according to Storm (2016a, 2016c) the crucial imbalance of the Eurozone.

Storm does not deny the existence of German wage restraint, to which he ascribes a weakening of domestic demand and, even more crucially, the decision of the ECB to adopt a low interest rate policy that presumably suited Germany, even if it led to credit bubbles in the periphery. However, wage restraint was, at best, a secondary actor in the drama, in which German productivity played the key role. By this token, the desirable policy for Europe would be some kind of strategy to strengthen productivity and thus competitiveness in the periphery, undercutting the German advantage and restoring balance. Presumably, the EMU and the EU would then be rescued.

The most that can be said in favor of this story is that it is well-meaning. For it lacks substance, coherence and relevance. Pretty much the same conclusion has been reached by economists as diverse as Bofinger (2016) and Bibow (2016). Wishing to oppose the mainstream is a laudable aim, but it cannot be done by sowing confusion. Even worse, the claim that Germany has come to dominate the EMU through its excellence in productivity is actually very similar to what Berlin continues to argue. To be sure, the German government does not favor a common investment strategy for Europe to buttress productivity in the periphery. The likelihood of the latter happening, after all, is similar to that of snow in Madrid in August. But if the crisis in the EMU pivots on putative German superiority in productivity, as Storm claims, then Berlin has drawn the obvious policy conclusion: the periphery must reform, restructure, and liberalise to improve its productivity and competitiveness.

In sharp contrast, the explanation of the crisis that stresses divergences in nominal unit labor costs due to German wage restraint does not allow for such conclusions. Not only is the current drive by Berlin and Brussels for “reforms” to increase productivity in the periphery ruthlessly destructive, it is also largely pointless. For, as long as German wage restraint perseveres, the fundamental imbalances of the EMU would not be remedied. Indeed, German wage moderation has persisted for far too long for the EMU to be able to survive in its current form, if at all. Although it would certainly be desirable to abandon wage restraint in Germany, that would no longer save the periphery, and nor would it rescue the EMU. Drastic action is now required, which means rapid exit for at least Greece and Portugal, and perhaps the organised dismantling of the EMU. The monetary union has failed and the culprit is Germany.

Heterodox voices in Europe certainly need conviction in the face of the austerity bandwagon, but they need clarity even more. Servaas Storm has conviction, yet his analysis throws the baby out with the bathwater. There could be no coherent explanation of Eurozone failure that left diverging nominal unit labor costs out of account. Consider the following.

What Is and What Is Not Neoclassical in Analysing Monetary Unions

In a rejoinder to us Storm (2016c) made the point that the analysis we have offered is a version of a neoclassical textbook model of a currency union. What a strange statement, and what could it possibly mean? Note that Keynes (1929) was also accused of being neoclassical in his famous analysis of the transfer problem following the First World War, which was actually very similar to the current problem of the Eurozone.

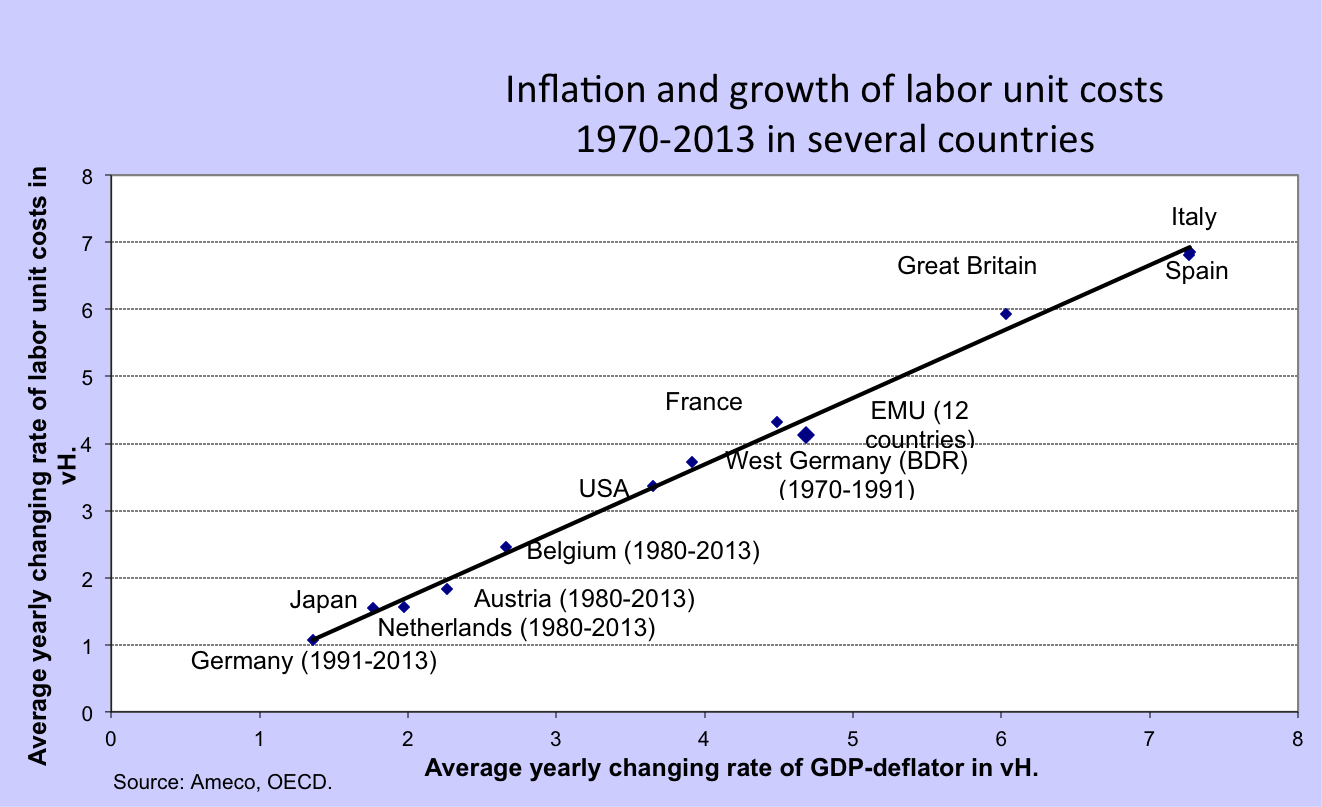

In our joint work (Flassbeck and Lapavitsas, 2013 and 2015) we have shown that Germany is the key wrongdoer and violator of the Maastricht Treaty. The most important argument in establishing this point is anything but neoclassical. To be specific, our analysis relies on the claim that, in the long run, inflation is more closely correlated to nominal unit labor costs than to anything else. Contrary to neoclassical thinking, the money supply or other putative correlates of inflation, exhibit a much weaker relationship with changes in the price level. Furthermore, and again completely different to the erroneous and misleading theory of Optimal Currency Areas, we have claimed that the most important rule for a monetary union to work is that all member countries should stick to the inflation target.

The evidence for the approach we have adopted is overwhelming and undeniable, as Chart 1 shows:

Chart 1 ULC and Inflation

Once it is acknowledged that nominal unit labor costs, rather than monetary aggregates, are the closest correlate to inflation in a single country as well as in a monetary union, there could be no reasonable doubt that Germany has been delinquent due to extraordinary wage restraint. Needless to say, peripheral countries have also diverged from the ECB target, in the opposite direction. Given its relative size and the persistence of the divergence, however, Germany’s policy has had disastrous implications for the EMU.

This conclusion provides a firm foundation for any rational analysis of the Eurozone crisis. Moreover, it does not deny the importance of other factors in exacerbating the Eurozone crisis during the same period, including capital flows, on which more will be said below. Above all, the conclusion is independent of any putative distortions to economic activity associated with German wage dumping. In this light, Storm’s emphasis on expenditure switching and the role of aggregate demand are largely irrelevant digressions, as was also made abundantly clear by Bibow (2016).

“Beggar-Thy-Neighbour” by “Beggaring-Thy-Own-People”

The real analytical issue in this regard is: how was it possible for wage restraint to become such a powerful instrument of EMU domination for Germany? The point to remember is that examining the impact of wage restraint on a country’s export performance is entirely different to examining its impact on the domestic economy. From this standpoint, there could be no doubt that a large country with intense trade relations would have the ability to “beggar” its neighbours through a real depreciation.

Storm (2016c) appears to accept this point but attributes it to exceptional Germany productivity performance rather than nominal wage restraint. Specifically:

“It is nevertheless true that Germany’s unit labor cost declined relative to those of the rest of the Eurozone … but this was not a result of wage restraint: It was completely due to Germany’s outstanding productivity performance.”

This claim is nonsensical as the two elements that form unit labor cost, i.e., nominal wages and productivity, cannot be separated in the way suggested by Storm. In a currency union, countries with high productivity performance must allow for higher wage growth to equalise unit labor cost growth, thus making the union sustainable in the absence of exchange rate changes.

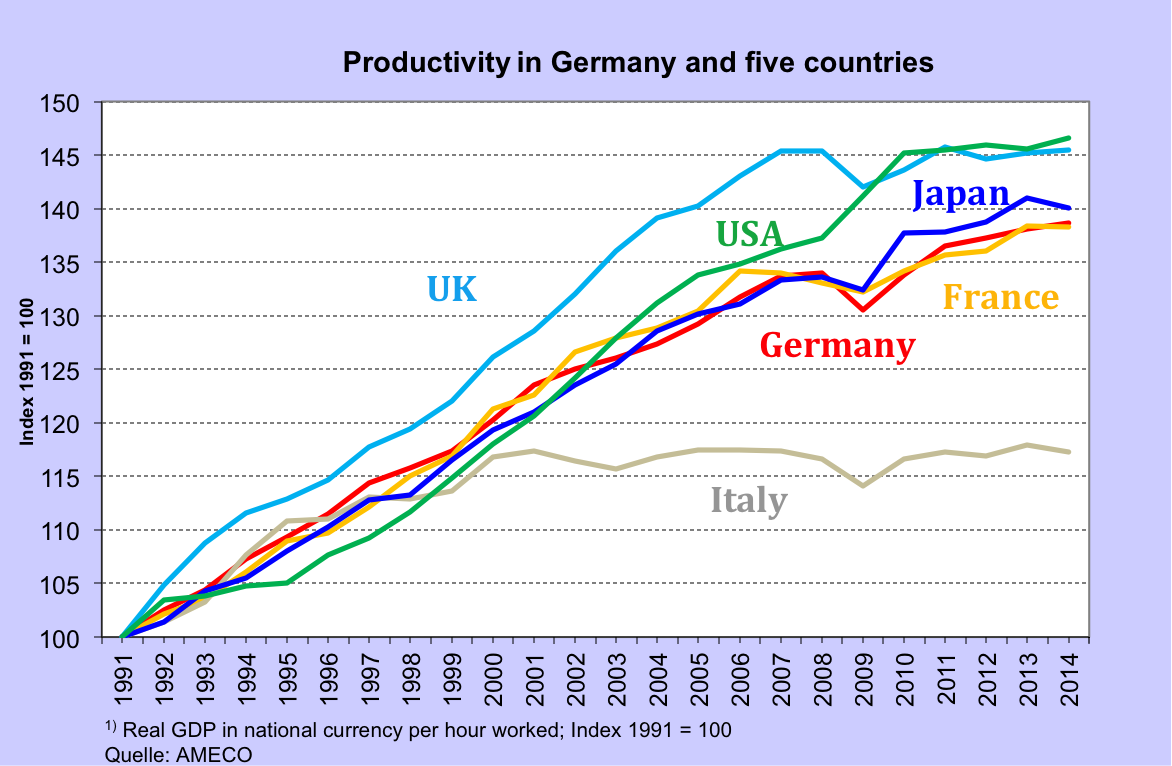

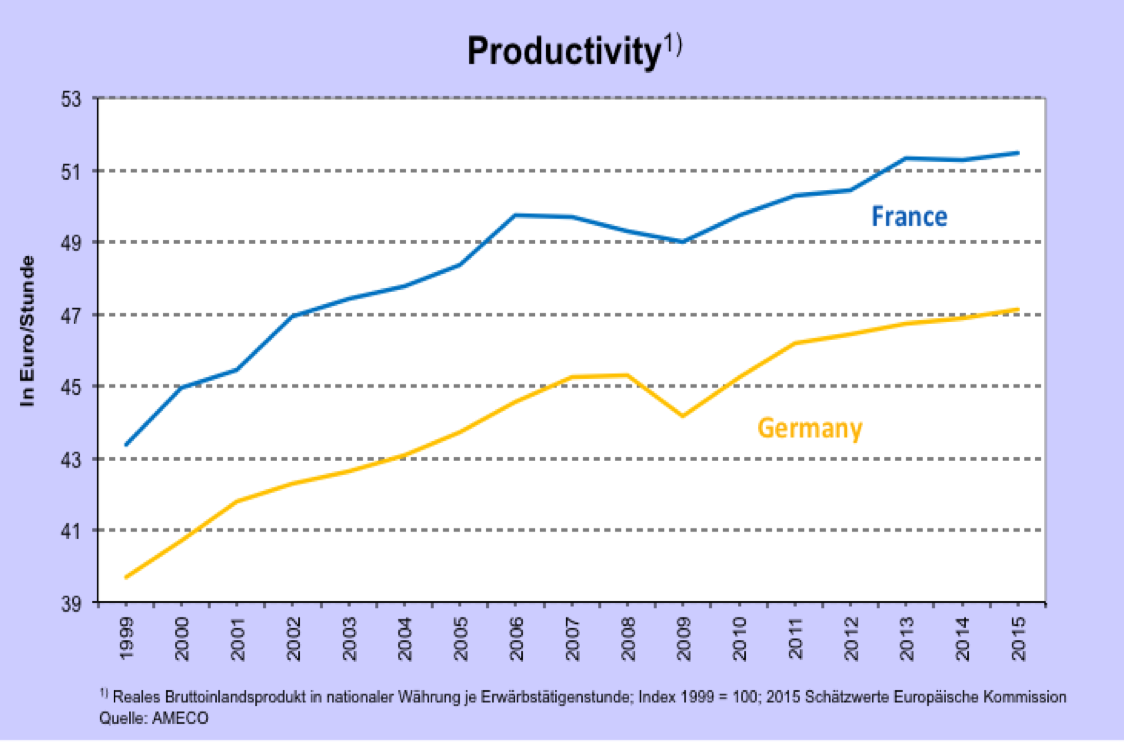

Even leaving the theoretical argument aside, however, Storm’s emphasis on the supposedly superior German productivity performance is wrong in factual terms. Chart 2 shows that, taking Storm’s preferred measure of productivity in terms of output per hour worked, there has been nothing “outstanding” about German performance globally. The decisive comparison in this regard is France, another core EMU country, which has been far more disciplined than Germany in meeting the inflation target of the ECB. Chart 3 shows that France’s labor productivity is higher that Germany’s in absolute terms, and the evolution of productivity in France and Germany has been very similar since 1999.

Chart 2 Productivity index

Chart 3 Productivity in Germany and France

There has been absolutely no German “productivity miracle” that could explain the export triumph of Germany and its domination of the Eurozone. The real secret of German success is eye-watering wage restraint, through which Germany has secured an absolute advantage in competitiveness that has accumulated over time. The bigger the absolute advantage, the greater the gain in German market share in the global economy. The stupendous increase in Germany’s export share in GDP and its rising export surplus reflect an unprecedented and unrepeatable explosion of competitiveness through wage restraint.

In sum, Germany has effectively “beggared” its neighbours, essentially robbing them of significant market shares in regional and global trade. This turn of events was made possible, first, because German workers were themselves “beggared”, allowing the gains of productivity to go entirely to capital and, second, because Germany’s trading partners accepted this form of economic imperialism and did not undertake retaliatory action. [2]

Against this conclusion, Storm (2016c) has also deployed the argument that empirical work shows that the price elasticities of German exports are small. The implication is that German export success was presumably determined by factors other than price competitiveness gains due to wage restraint. Once again, Storm has missed the point. If indeed German exporting enterprises were able to reflect lower unit labor costs in lower export prices but the price elasticities of German exports were low, the only outcome would be to delay the negative effect on trading partners. Put differently, the pain of wage dumping might be felt quickly by trading partners, if elasticities were high, or it might perhaps be delayed for a long time, if elasticities were low – assuming that no countervailing action was taken in the meantime. In the long run, however, elasticities would make no difference at all: the trading partners would have to adjust to the loss of competitiveness.

A simple mental experiment would further support this point. Suppose that for a period German enterprises were totally unable to pass lower unit labor costs onto export prices. In that case there would be nothing to measure in terms of elasticities. Yet, the profit margins of German exporting enterprises would be consistently higher than that of competitors, thus making it possible to succeed in the export markets through non-price techniques and measures.

The most important effect of real devaluation is to create fresh opportunities for economic agents. If the real exchange fell in a country with a diversified production structure and established trade ties, its enterprises and skilled workers would quickly grasp the opportunities presented by substantially lowered export prices occurring overnight; equivalently, they would grab the opportunity of making large extra profits at given prices.

Whether the results of the opportunities created by a real devaluation actually appear in this year’s GDP statistics or in next year’s export performance is an open question. If, for instance, the extra profits were used to improve the quality of the product – a strategy that German car-makers have deployed to good effect following real depreciation within the EMU – the beneficial effect could be truly long-term, even if short-term elasticities look modest. The benefit would still accrue to Germany.

The benefits, however, have not accrued to German workers, or to the German people in general. The strategy of wage restraint was originally intended to stimulate employment by changing relative factor prices as well as by restructuring production in the direction of labor intensive processes. This strategy did not succeed because – contrary to the neoclassical thinking that supported it – a slowdown of wage growth would inevitably be followed by a fall in domestic demand.

Specifically, wage restraint would immediately reduce aggregate demand by workers’ households; as aggregate demand by wage earners fell, enterprises would become unwilling to invest, even though new investment would be absolutely necessary to restructure production in light of the new relative prices of labor and capital; even worse, with falling demand and declining capacity utilisation of the existing capital stock, investment in fixed capital would also tend to fall, thus weakening domestic demand further. The end result would typically be a rise, rather than a fall, in unemployment.

This is precisely what happened to Greece, Portugal and Spain once the bailout programmes of the troika forced cuts in wages. Pressure on nominal wages started in 2008, with the real wage per hour falling in absolute terms from 2010 onwards. After 2010, and given the absolute reduction in real wages, unemployment continued to rise at nearly the same pace as during the global crisis. This could only have been a result of the immediate contraction of aggregate demand following the decline in real wages. Instead of pricing themselves back into the market, workers found themselves unemployed because they could not no longer buy the products they were producing.

A similar process occurred in Germany as domestic demand remained flat for several years reflecting stagnation in real wages. The saving grace of Germany, however, was its extraordinary success in international trade, which buttressed employment in spite of the weakness of domestic demand. The policy failed, but Germany was rescued by “beggaring” its neighbours and exporting its own unemployment.

Banks and Capital Flowing From Surplus to Deficit Countries

Finally, we come to capital flows and banks, Storm’s preferred culprits for the Eurozone crisis. Contrary to what Storm suggests, we have not in the slightest ignored the role of capital flows and banks in the Eurozone crisis, and have indeed discussed them in a series of publications. [3] It is a matter of record that capital flowed substantially from Germany and France to peripheral countries in the 2000s. It is also a matter of record that German and French banks were heavily involved in this process, and did not exactly cover themselves in glory in terms of delivering the basic banking functions of screening and monitoring borrowers. In fact, they failed abysmally. Much of their lending, furthermore, was to other financial institutions in the periphery.

The point is, nonetheless, that capital flows, credit and banks were not the primary causes of the crisis; that honour belongs to divergences in competitiveness. The Eurozone crisis was neither a crisis of credit overextension, nor a crisis of liquid capital flowing into peripheral countries to induce bubbles and resource misallocation. In this respect too, Storm is quite simply wrong in both theory and empirical substantiation. And since theory has been mentioned, Hilferding, who makes an entirely unexpected appearance in Storm’s narrative, never proposed a theory of “monopoly finance” and never suggested finance-related modes of competition among capitalist enterprises. In his time the world market was characterised by trade tariffs, which were the defining aspect of competition. Hilferding indeed believed in “organised capitalism”. If anything, this is the opposite of the contemporary world. [4]

In analysing the effects of the low interest rate policy of the ECB in the 2000s, it is vital to bear in mind that the divergence of nominal unit labor costs – and therefore of inflation rates (higher at the periphery, lower at the core and especially Germany) – meant that real interest rates were actually higher at the core throughout this period. In this light, it would have been a very strange form of financial capital that would have chosen to flow from core to periphery thereby causing bubbles in the latter. There were certainly flows from core to periphery but the economics of both capital flows and credit expansion were far more complex than in Storm’s account.

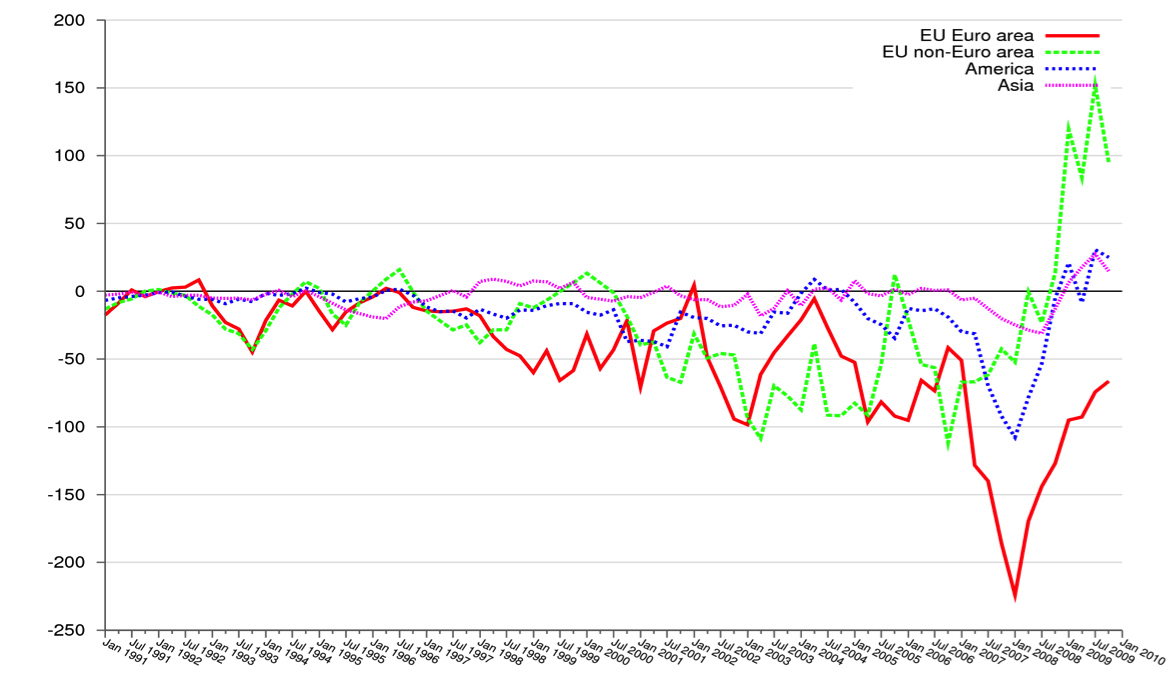

Consider Chart 4 which shows the regional composition of German ‘other’ outward flows over the 1990s and 2000s, i.e., essentially of international lending by German banks. Loans to what became the Eurozone were completely insignificant in the first part of the 1990s; became sizeable in the second half of the 1990s; grew with major fluctuations during 2001-6; and exploded in 2007. The violent reversal of the flows of German bank lending in 2008 signalled the start of the Eurozone crisis. In this regard what happened in the Eurozone after 2008 was a common-or-garden financial crisis, witnessed many times in developing countries as external credit flows dried up. The difference was, of course, that the reversal occurred within a monetary union, thus foreclosing the normal option of exchange rate devaluation. The inevitable adjustment occurred through wages, prices and output, and the outcome was catastrophic, nowhere more dramatically than in Greece.

CHART 4 German ‘other’ outward flows by region, Euro, bn

Bundesbank

What matters for our purposes is that the explosion of German bank lending to the Eurozone took place late in the 2000s, and mostly as a reaction to the unfolding global crisis. The first signs of crisis in the US mortgage market occurred in the summer of 2006; by the summer of 2007 the US real estate bubble was in full retreat. German (and other core Eurozone) banks turned to the Eurozone in the foolish belief that such lending was secure. By then, however, the real estate bubble in Spain and Ireland as well as the strong growth of credit in Greece had been in full swing for several years.

In short, the main culprit of credit expansion in the periphery were local financial institutions that took advantage of ECB interest rates, which were low historically for peripheral countries but also low compared to real rates in core countries. Spanish banks expanded Spanish credit in the direction of real estate and consumption, while Greek banks expanded Greek credit to finance a variety of activities, although there never was a real financial bubble in Greece.

The substance of credit growth was not capital flowing into Spain, or Greece from Germany as German lenders sought profitable opportunities abroad. Actually, domestic institutions expanded domestic credit, while taking the opportunity to borrow in the homogeneous money market of the Eurozone, sustained by the ECB. Peripheral banks were prepared to pay the going market rate to core banks, even if real interest rates were comparatively lower in the periphery. Peripheral banks expected domestic speculative profits easily to compensate, and for a while they were right. The price was paid later, but not by the banks and their owners.

External indebtedness, meanwhile, increased for Greece, Spain and Portugal, as it inevitably does when a current account deficit occurs due to loss of competitiveness and has to be financed. That is the normal way for the books to balance. The indebtedness took a variety of forms reflecting local conditions, being primarily public in the case of Greece and private in the case of Spain and Portugal. Quite naturally the debt was mainly owed to the surplus countries, that is, to Germany in the first instance.

The credit explosion in the peripheral countries was certainly important to the Eurozone crisis but not for the reasons Storm suggests. Its importance lay in masking the deleterious impact of the loss of competitiveness by creating a false sense of prosperity and giving the impression that the traditional concerns about current account deficits belonged to the past. How else to explain the astonishing fact that Greece had registered a current account deficit of 15% of GDP by 2008 without a serious policy alarm in the country and in the EU more generally?

In conclusion, a coherent analysis of the Eurozone crisis that retains a strongly critical and heterodox outlook ought not to get lost in thickets of analytical and empirical confusion. Opposing the orthodoxy does not mean devising an economics without foundations. The fundamental problem of Europe has sprung from current account imbalances generated by a tremendous gain of competitiveness for Germany. The cause of the gain in competitiveness was a shift in the balance of power between capital and labor in Germany, in favor of capital. Wage restraint for several years within the restrictive confines of the EMU did the rest. Finance played an important role in the disaster, but was secondary to the key processes.

If the debate on the causes of the Eurozone crisis that has recently broken out helps to establish this fundamental view among critical economists, it might be possible to develop a coherent analysis of what needs to be done now in Europe. This would indeed be a contribution by Servaas Storm.

REFERENCES

Bibow, J., 2016, How to Make a Mess of a Monetary Union, and of Analyzing It Too, Feb. 12, Multiplier Effect, The Levy Economics Institute Blog, http://multiplier-effect.org/how-to-make-a-mess-of-a-monetary-union-and-of-analyzing-it-too/, accessed on 16.2.2016.

Bofinger, P., 2016, Friendly Fire, INET, Jan. 20, http://ineteconomics.org/ideas-papers/blog/friendly-fire, accessed on 16.2.2016.

Flassbeck, H. and C. Lapavitsas, 2013, ‘The Systemic Crisis of the Euro: True Causes and Effective Therapies’, Rosa Luxemburg Stiftung Studien,

http://www.rosalux.de/fileadmin/rls_uploads/pdfs/Studien/Studien_The_systemic_crisis_web.pdf, accessed on 16.2.2016.

Flassbeck, H. and C. Lapavitsas, 2015, Against the Troika: Crisis and Austerity in the Eurozone, Verso: London and New York.

Flassbeck, H. and C. Lapavitsas, 2016, INET, Jan. 28, Wage Moderation and Productivity in Europe, http://ineteconomics.org/ideas-papers/blog/german-wage-moderation-and-the-eurozone-crisis-a-critical-analysis, accessed on 16.2.2016.

Keynes, J.M., 1929, “The German transfer problem,” Economic Journal, Vol. 39, No. 153, pp. 1-7.

Lapavitsas, C. 2013, Profiting without Producing: How Finance Exploits Us All, Verso: London and New York.

Lapavitsas C, and A. Kaltenbrunner, G. Lambrinidis, D. Lindo, J. Meadway, J. Michell, J.P. Painceira, J. Powell, E. Pires, A. Stenfors, N. Teles, and L. Vatikiotis, 2012, Crisis in the Eurozone, Verso: London and New York.

Storm, S., 2016a, German Wage Moderation and the Eurozone Crisis: A Critical Analysis, INET, Jan. 8, http://ineteconomics.org/ideas-papers/blog/german-wage-moderation-and-the-eurozone-crisis-a-critical-analysis, accessed on 16.2.2016.

Storm, S., 2016b, Response to Peter Bofinger’s “Friendly Fire”, INET, Jan. 20, http://ineteconomics.org/ideas-papers/blog/response-to-peter-bofinger, accessed on 16.2.2016.

Storm, S., 2016c, Rejoinder to Flassbeck and Lapavitsas, INET, Jan. 28, http://ineteconomics.org/ideas-papers/blog/rejoinder-to-flassbeck-and-lapavitsas, accessed on 16.2.2016.

ENDNOTES

[1] See Storm (2016a, 2016b, 2016c).

[2] The basic mechanism was explained by Keynes (1929).

[3] See Flassbeck and Lapavitsas (2013, 2015); see also Lapavitsas, et.al. (2012).

[4] One of us has written extensively on Hilferding. See, for instance, Lapavitsas (2013).