Progress in economics “is slow partly from mere intellectual inertia,” wrote Joan Robinson (1962, p. 79) long ago, because “[i]n a subject where there is no agreed procedure for knocking out errors, doctrines have a long life.” As a recent illustration of such inertia, it took more than five years since Eurozone crisis started full-force (in May 2010) to come to a more or less reasonable “consensus diagnosis” as proposed by a group of economists associated with CEPR (in “Rebooting the Eurozone,” published in

Vox on 20 November 2015).1

Even though this diagnosis marked a substantial advance, it invited strong critiques by Peter Bofinger (2015), one of the five members of Germany’s Sachverständigenrat, and from Oxford University’s Simon Wren-Lewis (2015).2 Both critics argue that the “consensus diagnosis” inappropriately focuses just on the deficit-crisis countries of Southern Europe, while neglecting the role of Germany, and of German wage moderation in particular, in bringing about the intra-Eurozone current account imbalances which are arguably at the heart of the Eurozone problématique.

The sad truth, however, is that Bofinger and Wren-Lewis are right for the wrong reason—hence their interventions are less than helpful, because rather than knocking out the remaining errors in the “consensus diagnosis”, they help perpetuate a mistaken doctrine: that relative unit-labor-costs matter are the prime determinant of a country’s international competitiveness, current account balance, and foreign indebtedness. The issue is serious: keeping alive the dangerous myth that labor costs drive “competitiveness” feeds the irrepressible urge of the orthodox mainstream to try to bring about economic recovery by reducing Eurozone unit labor costs (Gabrisch and Staehr 2014; Janssen 2015; Storm and Naastepad 2012, 2015b, 2015c). This intrinsically beggar-thy-neighbour strategy has already become codified into official Eurozone policy: in the Euro Plus Pact (adopted by the European Council in March 2011) and recently by the Informal European Council (February 2015), which both combine it with a prescription for fiscal austerity based on a tight cyclically-adjusted public budget constraint.3 It is therefore high time to look more closely at the labor cost competitiveness myth.

Progress: What the Consensus Diagnosis Gets Right

But first let me clarify that the consensus diagnosis is right in pointing out that the Eurozone crisis is not a sovereign debt crisis in its origin. Instead, it correctly holds that (i) the Eurozone crisis originated in a (banking) crisis of cross-border capital flows gone wild that led to massive intra-Eurozone (current account) imbalances; and (ii) that the crisis has been amplified by institutional flaws in the design of the Eurozone. The consensus authors rightly point to the vicious “doom loop” in which crisis-struck Eurozone governments, lacking access to a lender of last resort, were left to borrow only from their national banking systems—systems which had become increasingly insolvent and in turn had to be bailed out by the same governments. The diagnosis that the Eurozone crisis is a crisis of deregulated (too-big-to-fail) banking is consistent with earlier analyses by Lane (2012), Lane and Pels (2012), Gabrisch and Staehr (2014), Storm and Naastepad (2015c, 2015d), O’Connell (2015) and others.

It is a far cry from the orthodox diagnosis propounded by mainstream economists such Sinn (2014) and by the European Commission, which absolve TBTF banks from any responsibility for the crisis and instead blames the “victims,” arguing that profligate Southern European countries, by allowing nominal wage growth to persistently exceed labor productivity growth, let their relative unit labor costs increase and their cost competitiveness deteriorate. In this narrative, rising unit labor costs are due to fiscal profligacy and “rigid” “over-regulated” labor markets, powerful unions, and strong employment protection. Rising relative unit labor costs supposedly killed Southern Europe’s export growth, raised current account deficits, created unsustainable external debts and reduced fiscal policy space, and hence, when the crisis broke, these countries lacked the resilience to absorb the shock. It follows in this story that the only escape from recession is for the Southern European countries rebuild their cost competitiveness—cutting wage costs (because Eurozone members cannot devalue their currency) by as much as 30% (as proposed by Sinn 2014), which requires in turn that their labor markets be thoroughly deregulated.

The Flip Side: The “Unit-Labor Cost Competitiveness Matters” Myth

Bofinger is right: when it comes to individual countries, the “consensus diagnosis” one-sidedly focuses on the crisis-struck deficit countries of Southern Europe, while the role of the Eurozone surplus countries, and Germany in particular, in bringing about the imbalances is left unmentioned. This omission is even worse, because the “consensus diagnosis” promulgates the “official” party line by claiming (in a throw-away sentence) that “the rigidity of factor and product markets [in Southern Europe] made the process of restoring competitiveness slow and painful in terms of lost output.” The consensus diagnosis thus accepts the official remedy of internal devaluations and labor market deregulation imposed on the crisis-struck countries by the European Commission, the ECB and the IMF.

Bofinger and Wren-Lewis wish to set part of the record straight by highlighting Germany’s responsibility for bringing about the Eurozone crisis. They argue that Germany’s long-term policy of wage moderation (based on a deliberate voluntary tri-partite agreement between German employers, trade unions and government) undercut its Eurozone neighbours and thereby raised Germany’s labor-cost competitiveness, helping to cause the Eurozone crisis by contributing to the build-up of Eurozone (current account) imbalances. Southern Europe’s cost competitiveness problem, in other words, was created in Berlin. The result, as Bofinger (2015) argues, is that German domestic and import demand slowed down, while its increasingly more cost-competitive exports experienced fast growth; as a result, the profit share in German GDP increased simultaneously with a growing current account surplus.

Confusing “simultaneity ” with “causality,” Bofinger then suggests that the higher corporate profits were used to finance the (net) outflow of German savings to the rest of world, as indicated by its current account surplus.4 German wage moderation in this story is (mostly) to blame for the weakening of Southern Europe’s cost competitiveness as well as the large capital flow from Germany to the increasingly indebted and vulnerable Eurozone periphery. Wren-Lewis calls this the “untold story of the Eurozone crisis,” which is rather remarkable, because many authors made exactly the same point earlier including Lapavitsas et al. (2011), Stockhammer (2011), Bibow (2012), Flassbeck and Lapavitsas (2013) (for a lengthy list of references see Storm and Naastepad 2015a, 2015b, 2015c). These accounts show that wage moderation is a very powerful narrative (especially in Europe’s North), probably because it resonates with Calvinism and fits seamlessly with Weber’s Protestant Ethic, centring around the notion of “delayed gratification”: first the pain of tightening your belts to improve labor-cost competitiveness in order to obtain the gain of higher export growth, higher incomes and more jobs at a later stage. But, as Tolstoy (1882) wrote in A Confession, “wrong does not cease to be wrong, because the majority share in it.”

Knocking Out Errors

Bofinger’s narrative is worrisome in two major ways. First, by exclusively focusing on the real economy (wages, corporate profits, cost competitiveness and trade), the financial sector disappears from the scene—even though Bofinger seems to agree that the Eurozone crisis is in essence a financial crisis—and it becomes almost natural to only look for solutions in the real economy. In this way, the culprits (

i.e., TBTF banks) are let off the hook—which means the real origins of the imbalances and crisis are left undebated. Secondly, of course it is true that Germany and German wage moderation bear part of the responsibility for bringing about the Eurozone crisis. Bofinger and Wren-Lewis have the best intentions while making this point (alas, the road to hell is paved with good intentions ….), but their single-minded emphasis on the importance of relative unit labor cost competitiveness is misguidedfor at least the following three reasons.

Firstly, exports and imports are—by definition (as explained in Storm and Naastepad 2015a, 2015c)—much less responsive to changes in (relative) unit labor costs than to changes in (relative) prices for several reasons. Unit labor costs make up less than 25% of the gross output price, while a second reason is that firms in general do not pass on all (but mostly only half of) unit labor cost increases onto market prices. What it means is that (when using realistic unit-labor cost elasticities) observed changes in Germany’s relative unit labor cost statistically “explain” only a minuscule fraction of its export growth and current account surplus (Wyplosz 2013; Gabrisch and Staehr 2014). For instance, IMF economists Danninger and Joutz (2007, p. 15) find that relative cost improvements accounted for less than 2% of German export growth during 1993-2005. Germany’s superior export performance can instead be completely explained by the “income effect” (Storm and Naastepad 2015a): German firms supply mostly complex, high-tech, and high-priced goods to fast-growing markets as well as to faster-growing countries such as China, Russia and Saudi Arabia (Gabrisch and Staehr 2014; Diaz Sanchez and Varoudakis 2013; Storm and Naastepad 2015a; Schröder 2015). Germany excels in non-price (technology-based) competitiveness and does not engage (much) in price competition.

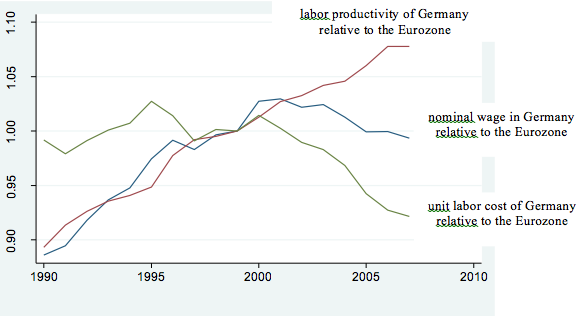

Secondly, as shown in Figure 1, there is no clear sign of a nominal wage squeeze on German workers if we compare Germany to the Eurozone as a whole (but excluding Germany). German nominal wages increased relative to the Eurozone in the 1990s and the German relative nominal wage stayed more or less flat during the period 1999-2007 (there was a negligible decline of 0.7 percentage points over these eight years). It is nevertheless true that Germany’s unit labor cost declined relative to those of the rest of the Eurozone (as Figure 1 illustrates), but this was not a result of wage restraint: It was completely due to Germany’s outstanding productivity performance: during 1999-2007 average German labor productivity (per hour worked) increased by almost 8 percentage points compared to the rest of the Eurozone, which accounts fully for the decline in Germany’s relative unit labor costs by 7.8 percentage points over the same period. It was German engineering ingenuity, not nominal wage restraint or the Hartz “reforms”, which reduced its unit labor costs. Any talk of Germany deliberately undercutting its Eurozone neighbors is therefore beside the point.

Thirdly, the increase in current account deficits in Southern Europe resulted from an increase in the trend growth of their imports, while the trend growth of their exports stayed unchanged (notwithstanding the sustained rise in their unit labor costs). There is convincing statistical evidence for the European Union (Diaz Sanchez and Varoudakis 2014; Storm and Naastepad 2015c) showing that initial increases in current account deficits were followed only later in time by increases in relative unit labor costs—which, if true, means that the current account deteriorations were not caused by higher (relative) unit labor costs. The only rational explanation for the observed time-sequence is that Southern Europe first experienced a debt-led growth boom, which then led to higher imports and higher capital inflows leading only after a lag of many quarters to lower unemployment and higher wage growth in excess of labor productivity growth (see Storm and Naastepad 2015c). This explanation is consistent with the first two statements of “consensus diagnosis” outlined above .

Figure 1

Nominal hourly wages, hourly labor productivity and unit labor cost:

Germany vis-à-vis the rest of the Eurozone (1990-2007; 1999 = 1.00)

Authors’ calculations from EU-KLEMS Database. See Storm and Naastepad (2015a). Relative unit labor cost is defined as the ratio of the relative nominal wage and relative labor productivity.

The Unmentioned Issues

The real problem of the Eurozone is, accordingly is not that unit labor costs have not converged but that the common currency and monetary unification have not led to a convergence of member countries’ production, employment, and trade structures, but rather to a centrifugal process of structural divergence in production. In a nutshell, since the mid-1990s, Germany has become stronger and more productive in high-value-added, higher-tech manufacturing (in conjunction with outsourcing to Eastern European countries), while Southern European countries became more strongly locked into lower-tech, lower value-added and, often, non-tradable activities (Storm and Naastepad 2015c). This has reinforced the core-periphery relationship between Germany and the Southern-European countries—meaning that Southern European growth spills over into German growth (via trade and finance) but not vice versa (Janger et al. 2012; Simonazzi, Ginzburg & Nocella 2013; Botta 2014; O’Connell 2015). This centrifugal process has been fueled and strengthened not just by the surge in cross-border capital flows following the introduction of the euro, but also by the common currency itself (as argued by Wierts, van Kerkhoff and de Haan 2014) as well as by the centralized and uniform interest rate policy of the ECB which up to 2008 was perhaps appropriate for stagnant and low-inflation Germany, but was undeniably out-of-sync with inflation levels in Southern Europe (Storm and Naastepad 2015c). Cheap credit in the South created unsustainable asset bubbles and facilitated untenable debt accumulation which fed into higher growth, lower unemployment and higher wages—but all concentrated in the non-dynamic and often non-tradable sectors of their economies.

In this analysis, the role of German wage moderation is very different from conventional wisdom. It mattered a lot, not through its supposed impact on cost competitiveness, but via its negative impacts on demand or, more specifically, (wage-led) German growth and inflation, which in turn prompted the ECB to lower the interest rate excessively for the Eurozone as a whole (as is illustrated in Storm and Naastepad 2015c, by Figure 1). The real issues facing the Eurozone have nothing to do with wages, cost competitiveness or trade imbalances. They are instead how to bring about a structural convergence between member countries of a common currency area (so far lacking any meaningful supranational fiscal policy mechanisms) in terms of productive structures, productivity levels, and ultimately incomes and long-term living conditions—which certainly will not be achieved by cutting wages and deregulating labor markets? What is the appropriate interest rate for the structurally divergent “core” and “periphery” in a one-size-fits-all monetary union? And how can banks, the financial sector and capital flows be made to contribute to a process of convergence (rather than divergence)?

These are hard nuts to crack —but let us hope that it will not take another five full years to finally ditch the dangerous myth that unit labor cost competitiveness is the prime problem and come up with a more rational Eurozone macro policy than the self-destructive policies of internal devaluation” and “structural reforms” pursued so far.

Bibliography

Bibow, J. 2012. The euro debt crisis and Germany’s euro trilemma. Working Paper No. 721. Levy Economics Institute of Bard College.

Bofinger, P. 2015. German wage moderation and the Eurozone crisis. Social Europe. 1 December. At: http://www.socialeurope.eu/2015/12/german-wage-moderation-and-the-eurozone-crisis/

Botta, A. 2014. Structural asymmetries at the roots of the Eurozone crisis: What’s new for industrial policy in the EU. Levy Economics Institute of Bard College Working Paper No. 794.

Costantini, O. 2015. The cyclically adjusted budget: history and exegesis of a fateful estimate. INET Working Paper No. 24. Available at: http://ineteconomics.org/uploads/papers/WP24-Costantini.pdf

Danninger, S. and F. Joutz. 2007. What explains Germany’s rebounding export market share?, IMF Working Paper WP/07/24. Washington, DC: IMF.

Diaz Sanchez, J.L. and A. Varoudakis. 2013. Growth and competitiveness as factors of Eurozone external imbalances. World Bank Policy Research Working Paper 6732. Washington, DC: World Bank.

Flassbeck, H. and C. Lapavitsas 2013. The Systemic Crisis of the Euro – True Causes and Effective Therapies. STUDIEN, Berlin: Rosa-Luxemburg-Stiftung.

Gabrisch, H. and K. Staehr. 2014. The Euro Plus Pact: cost competitiveness and external capital flows in the EU countries. ECB Working Paper Series No. 1650. Frankfurt: European Central Bank.

Informal European Council. 2015. Preparing for the Next Steps on Better Economic Governance in the Euro Area. Analytical Note written by J.-C. Juncker, D. Tusk, J. Dijsselbloem and M. Draghi. Brussels: European Commission.

Janger, J., W. Hölzl, S. Kaniovski, J. Kutsam, M. Peneder, A. Reinstaller, S. Sieber, I. Stadler, and F. Unterlass. 2011. Structural Change and the Competitiveness of EU Member States - Final Report. On-line available at: http://ec.europa.eu/enterprise/policies/ industrial-competitiveness/documents/files/structural_change_en.pdf

Janssen, R. 2015. European economic governance and flawed analysis. Social Europe. Available at: http://www.socialeurope.eu/author/ronald-janssen/

Lane, P.R. 2012. The European sovereign debt crisis. Journal of Economic Perspectives 26 (3): 49-68.

Lane, P.R. and B. Pels. 2012. Current account imbalances in Europe. IIIS Discussion Paper No. 397. Trinity College Dublin.

Lapavitsas, Costas et al. 2011. Breaking Up? A Route Out of the Eurozone Crisis. RMF Occasional Report 3. November. Research on Money and Finance.

O’Connell, A. 2015. European crisis: a new tale of center–periphery relations in the world of financial liberalization/globalization? International Journal of Political Economy 44 (3): 174-195.

Rebooting Consensus Authors. 2015. Rebooting the Eurozone: Step 1 – agreeing a crisis narrative. 20 November. Available at: http://www.voxeu.org/article/ez-crisis-consensus-narrative

Robinson, J. 1962. Economic Philosophy. London: Penguin Books.

Schröder, E. 2015. Eurozone imbalances: measuring the contribution of expenditure switching and expenditure volumes 1990-2013. Department of Economics Working Paper 08/2015, The New School for Social Research. Available at: http://www.economicpolicyresearch.org/econ/2015/NSSR_WP_082015.pdf

Simonazzi, A., A. Ginzburg and G. Nocella. 2013. Economic relations between Germany and southern Europe. Cambridge Journal of Economics 37 (3): 653-675.

Sinn, H.W. 2014. Austerity, growth and inflation: remarks on the Eurozone’s unresolved competitiveness problem. The World Economy 37 (1): 1-13.

Stockhammer, E. 2011. Peripheral Europe’s debt and German wages. The role of wage policy in the Euro Area. Research on Money and Finance Discussion Paper No. 29.

Storm, S. and C.W.M. Naastepad. 2012. Macroeconomics Beyond the NAIRU. Cambridge, Mass.: Harvard University Press.

Storm, S. and C.W.M. Naastepad. 2015a. Germany’s recovery from crisis: The real lessons. Structural Change and Economic Dynamics 32 (1): 11-24. http://www.sciencedirect.com/science/article/pii/S0954349X15000028

Storm, S. and C.W.M. Naastepad. 2015b. Europe’s Hunger Games: income distribution, cost competitiveness and crisis. Cambridge Journal of Economics 39 (3): 959-986.

Storm, S. and C.W.M. Naastepad. 2015c. NAIRU economics and the Eurozone crisis. International Review of Applied Economics 29 (6): 843-877.

Storm, S. and C.W.M. Naastepad. 2015d. Myths, mix-ups and mishandlings: understanding the Eurozone crisis. At: http://ineteconomics.org/ideas-papers/research-papers/myths-mix-ups-and-mishandlings-what-caused-the-eurozone-crisis

Wierts, P., H. van Kerkhoff and J. de Haan. 2013. Composition of exports and export performance of Eurozone countries. Journal of Common Market Studies 52 (4): 928-941.

Wren-Lewis, S. 2015. Was German undercutting deliberate? Social Europe. December 4. At: http://www.socialeurope.eu/2015/12/was-german-wage-undercutting-deliberate/

Wyplosz, C. 2013. Eurozone crisis: it’s about demand, not competitiveness. At: https://www.tcd.ie/Economics/assets/pdf/Not_competitiveness.pdf

- 1. http://www.voxeu.org/article/ez-crisis-consensus-narrative

- 2. http://www.socialeurope.eu/2015/12/german-wage-moderation-and-the-eurozone-crisis/ and http://www.socialeurope.eu/2015/12/was-german-wage-undercutting-deliberate/

- 3. See Costantini (2015) for a hard-hitting exegesis of cyclically-adjusted budgetary policy, which traces its evolution from an essentially Keynesian concept in the 1940s, '50s and '60s, to a dogmatic New-Classical and (within the Eurozone) an Ordo-Liberal concept today.

- 4. The simultaneous increases in corporate savings and net capital outflows from Germany are not directly linked. Net capital outflows are the result of gross cross-border capital flows, which in turn are determined (even "pushed") by events in the countries (such as Germany) where the large financial institutions channeling the lending are based (O'Connell 2015). This means gross capital flows are not necessarily (or at all) related to the financing of trade. For example, Germany was Ireland's biggest net creditor by far, but only a minor Irish trading partner. O'Connell (2015) convincingly argues that the Eurozone crisis is a creditors' crisis.