In the following I will summarize some of the points and their policy implications, which I find of particular interest, and comment on possible implications for economic policy in the Eurozone. Subsequently, I will touch on two broader and somewhat heterodox questions that arise in connection with Blanchard’s analysis, concerning the effectiveness of monetary policy and the NAIRU.

The Phillips Curve: back to the 1960s

Some of the major empirical results reported in Blanchard et al (2015) and Blanchard (2016), based on data for 20 industrial countries in the period 1960- 2013 can be schematized as follows:

a) Deviations of the unemployment rate from the NAIRU determine a change in the level of inflation. The relationship therefore goes from the level of unemployment to the level of inflation and looks like the old, 1960s, downward sloping Phillips Curve (Blanchard 2016, p. 1); in addition, the relationship is weak as the large standard error of the residuals testifies. (Blanchard 2016, p. 1)

b) The Phillips Curve is currently rather flat, and it has been so since the 1990s – hence large changes in the unemployment rate are necessary to bring about significant changes in inflation (Blanchard 2016, p. 3). The coefficient linking unemployment to inflation moreover tends to be inversely related to the level of unemployment (Blanchard et al, 2015, p. 24).

c) There is hysteresis in output (Blanchard et al, 2015, pp. 5-18); this, along with the small coefficient mentioned above, implies that the Central Bank objectives should include not only price stability but also unemployment, since stabilization policies may have significant costs in terms of high and persistent unemployment (Blanchard et al, 2015, p. 25; Ball, 2015, p. 48).

Point a) is explained, according to Blanchard, by hysteresis and by the fact that currently a low weight is attached to lagged actual inflation in forming price expectations. This in turn may be attributed both to low inflation and to the greater credibility than in the past of central banks’ declared targets. Accordingly, Blanchard is very cautious about the policy implications, as he fears that changes in the monetary policy might alter the way expectations are formed and bring back the accelerationist Phillips Curve (Blanchard, 2016, p 4). Yet, the weakness of the relationship suggests that some change in unemployment could occur without consequences even for the level of inflation.

Points b and c appear to be of particular relevance for the Eurozone policies and institutions. The latter is clearly in contrast with the statute of the European Central Bank that, unlike the US Federal Reserve, defines its objectives only in terms of price stability (on this, Ball, 2015, p. 49). But the former (point b) questions most strongly the current European policies, for the two following reasons.

The first is that the attempt to restore competitiveness in the periphery by pursuing internal devaluation, with lower output and higher unemployment, may require output losses and unemployment of disastrous size – as in Greece – which with hysteresis may become persistent. Hence, restoring price competitiveness in the periphery can safely happen only with the contribution of higher inflation in the core (Ball, 2015, pp. 50-51). The other reason is that the statement in b) also means that, if the problem is not curbing inflation but, as is currently the case in the Eurozone as a whole, preventing deflation, then large falls in the unemployment rate are required in order to bring about a little bit of inflation even in the very moderate range of the ECB target of somewhat below 2%. On the basis of the estimated value 0.2 of the coefficient θ linking unemployment to inflation, with given expectations the unemployment rate should fall by 5 points in order to bring the inflation rate from 0 to 1%. (Blanchard 2016, p. 3)

This set of observations is very interesting since, ultimately, as emphasized by Ball, it goes against the conventional wisdom that prevails in textbooks as well as in policy making, that market forces themselves will bring output and employment to their natural path, quite independently of the recessions and their causes (Ball, 2015, p. 47). However, at the same time, it raises broader and more radical questions, two of which I shall try to briefly outline below. The first one is how far monetary policy alone can successfully pursue unemployment and inflation targets, the second concerns the role of the NAIRU and alternative interpretations of the Phillips Curve.

Can monetary policy deliver low unemployment?

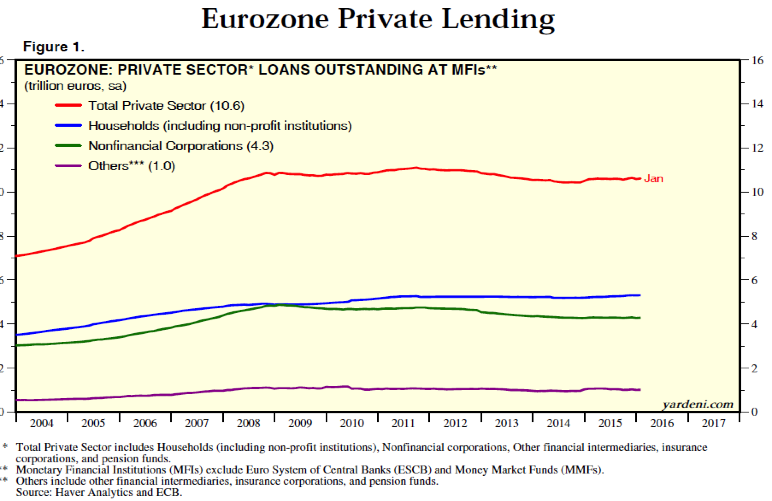

It is increasingly worrying for the Eurozone that Quantitative Easing has not, up to now, been able to deliver higher inflation (or at least no deflation). According to Blanchard’s analysis and empirical findings, in order to do so monetary policy should be able to generate a significantly lower unemployment rate in the Eurozone. The question therefore is what are the channels through which monetary policy is supposed to achieve these goals. According to standard textbook macro, low interest rates (and/or wealth effects) should stimulate credit demand on the part of consumers (that is, demand for mortgages and consumer credit) and firms (to finance increasing investment). But several studies have shown that interest rates have little or no impact on investments (Blanchard, 1986; Chirinko, 1993; Ford and Poret, 1990; Khotari et al 2014; Sharpe and Suarez, 2014) and some of them point to changes in output (aggregate demand) as their main driver (on this, see also Fiebiger, 2014; Girardi and Pariboni, 2015; Hillinger, 2005; Onaran e Galanis, 2012; Shoder, 2014; Stockhammer et al, 2011; Wen, 2007). Thus, transmission to the real economy should mainly come through consumer credit and mortgages. There may be many reasons however for this channel not to work in the currently prevailing conditions, in which the private sector is deleveraging, gloomy employment and income prospects may encourage a higher propensity to save and prices in the real estate sector may be expected to continue falling. Also, on the credit supply side, the banking sector may be more reluctant than in the past to lend to the private sector for several reasons, among which the fact that it has become riskier in peripheral countries owing to economic recession, plant closures, and poor prospects concerning employment and households disposable income. Indeed data show that lending to the private sector has not increased (Figure 1).

Another channel of monetary policy transmission is that lower interest rates on public bonds might make room in public budgets for more expansionary types of expenditures than interest rate payments, and also encourage more deficit spending. These effects however are in turn constrained by balanced budget targets and commitment to curb public debts.

Up to now, an important channel has been the exchange rate devaluation vis à vis the dollar – but it is doubtful that this result can be persistent, and that it could have the required large impact on unemployment.

Just recently, Draghi announced new measures, and remains to be seen what their impact will be. Based on the above mentioned studies on investments, however, there are no reasons to believe that they will be able to provide the required stimulus.

In addition, internal devaluations pursued in peripheral countries, with cuts in nominal wages and public spending, are clearly in sharp conflict with the no-deflation target of the ECB and with a fall in unemployment (see e. g. the analysis of fiscal multipliers in Blanchard and Leigh, 2013). Actually, the Euro-area as a whole appears to suffer badly from a lack of coordination between monetary and fiscal policy.

Thus, while in general the ability of monetary policy to stimulate the economy is more limited than in textbook accounts, due to its limited or nil effect on investments, in Europe, today, its weapons are simply ineffective, unless a major turn in macroeconomic policies takes place and monetary policy becomes instrumental to a large scale financing of public expenditure and investments.

Figure 1

Source: Yardeni, Johnson, Quintana, 2016

The elusive concept of the NAIRU: an alternative perspective

Another major question that arises from Blanchard’s analysis is whether the NAIRU should (or can) still be regarded as a relevant concept in guiding macroeconomic policies (see also Ball, p. 47). In fact, if ‘hysteresis’ in output and unemployment is pervasive, stable inflation can be associated to different unemployment rates and the NAIRU varies together with actual unemployment, what is the purpose or, even, the significance of the concept? To better focus on this question, it is useful to compare its theoretical underpinnings, which still are at the basis of its role in policy-making, and its empirical counterpart. The tensions between the two may suggest it is time to turn to a different interpretation of the unemployment-inflation relationship and of hysteresis.

The NAIRU in theory

In the original empirical work by Phillips, the average unemployment rate (after adjusting for the cycle) was found to be associated with different money wage (and price) inflation rates. This however was at variance with the accepted wisdom that inflation necessarily arose from a condition of excess demand in labour and goods market. The relationship had to be re-interpreted according to received theory: positive inflation became associated with excess demand and with an unemployment rate below equilibrium, causing upward pressures on the real wage.

From this, the accelerationist view necessarily follows on logical grounds, since existing inflation must sooner or later become incorporated into expectations which affect the process of wage determination. The downward Phillips Curve becomes reinterpreted as a short-run relationship, [1] shifting with changes in expectations, while in the long run stable inflation must require that the economy is in equilibrium and is therefore at the natural unemployment rate or NAIRU. This is the basis of what Blanchard calls the ‘divine coincidence’ by which at the NAIRU stable inflation goes along with the maximum employment which can be attained given the existing structural constraints (be they the intensity of frictions, the degree of information available to agents, or the institutions prevailing in the labour market and causing some real wage rigidity). All this however implies that the NAIRU is rather stable, that it is independent of actual unemployment rates, and that its changes can be explained by changes in its ultimate structural determinants.

The NAIRU in practice

While the accelerationist interpretation was empirically successful in the seventies, with time empirical estimates of the NAIRU proved to conflict with the theory: Firstly, they were soon found to vary a lot – as testified by the creation of the new concept of a time-varying NAIRU (see Blanchard, 2015, pp 21, 24; and the much cited work by Gordon, 1997). Secondly, attempts to explain its movements by changes in what, according to theory, are its underlying determinants, proved unsatisfactory. In fact, movements in the NAIRU appeared to follow those in actual unemployment. Blanchard and Summers and others started addressing this problem back in the 1980s, developing models with hysteresis. This approach was confirmed and accepted in many empirical studies. For example, research carried out at the OECD led already in the 1990s to the conclusion that: “despite considerable efforts, it has been hard to identify changes in the basic determinants of equilibrium unemployment large enough to account for the observed trend increase in actual unemployment. Consequently, the alternative hypothesis has been put forward that unemployment may be strongly dependent on its own history (‘hysteresis’). According to this view, current equilibrium unemployment is not independent of past actual unemployment [….] demand shocks end up having longer-term supply consequences” (Pichelmann and Schuh, 1997) . Similarly, empirical work showing that there is no connection between changes in the EPL (employment protection legislation) and the estimated NAIRU questions its dependence on ‘structural factors’ such as labour market institutions (see e. g. Baker et al, 2005).

To put it bluntly, but clearly, hysteresis means that we are back to the old, downward sloping relationship of the kind found by Phillips (different levels of unemployment rate are associated to different stable inflation rates). It also means, in practice, that the estimated time-varying NAIRU depends on the actual path of unemployment, and that changes in the unemployment rate tend to be persistent – that is, we do not observe a tendency of unemployment, after a recession (or a boom), to roll back to an ‘equilibrium rate’ which is determined independently of the recession (or boom) itself.

In practical terms, after a recession, the level of unemployment at which inflation is found to be stable is higher than its mere structural determinants would imply; or, according to models with hysteresis, the ‘structural determinants’ themselves are seen to depend on aggregate demand, in an arguably ad hoc manner. A case in point is changes in the share of long term unemployed in total unemployment, which is regarded in such models as a ‘structural factor’ behind the NAIRU. At any rate, the dependence of the estimated NAIRU on actual unemployment means that an increase in aggregate demand could significantly reduce it, changing the relation found at any time between unemployment and inflation.

But while all the different estimating techniques of the NAIRU nowadays imply, in differing degrees, such dependence on actual unemployment, [2] the policy implications do not seem to follow. In other words, recognition that the movements of demand matter more than, say, the degree of rigidity in labour markets does not lead to the conclusion that policies to support aggregate demand could appropriately address the problem of unemployment. That is, the idea that the so defined time-varying, path-dependent NAIRU corresponds to the natural equilibrium rate is not dropped.

Just to be concrete: the NAIRU is currently estimated by international institutions to be around 20% in Spain. Actually, it was predicted by research carried out at OECD, that “structural” unemployment would have increased in Spain (as in other countries) as a consequence of the crisis (Guichard and Rusticelli, 2010). And indeed it has, by far more than predicted: the increase in the currently estimated NAIRU is double than forecasted. Yet, the NAIRU and the associated concept of potential output are still regarded by European institution as useful guidance for policy. For instance, they are used to assess structural budget deficit constraints, which limit precisely the only action that could make a difference. So, in a sense, they are self-reinforcing.

But is it really possible to believe that an unemployment rate somewhat below 20% would cause accelerating inflation? Not really, on the basis of common sense and empirical evidence, including Blanchard et al. 2015. Ironically, even the European Commission sometimes admits that the NAIRU is “likely to overstate the magnitude of unemployment linked to structural factors,” and the current increase could be reversed, “should labour demand growth and labour market matching efficiency go back at pre-crisis levels” (European Commission, 2013, p. 90, quoted in Palumbo, 2015, p. 296). After all in the US, during the 1990s unemployment fell from 7% to 4%, while nominal wages of production workers increased at a roughly constant rate of 2% (Eurostat and BLS data).

Both hysteresis on the theoretical side and its methods of estimation on the empirical side appear to void the NAIRU of the relevance which, by contrast, it still holds in policy making. This does not mean to say that accelerating inflation cannot be brought about by low unemployment, but evidence suggests this would be the outcome of specific circumstances rather than the rule.

An alternative view

The above points to an inconsistency between the theoretical underpinnings of the concept of the NAIRU and its use in policy making as an equilibrium structural variable on the one hand, and empirical evidence on the other. Such inconsistency has been widely acknowledged for a long time, and ought to lead to a change in perspective.

Actually, a different tradition exists that interprets inflation and its connections with unemployment in ways that might be more consistent with the evidence. It is the view that inflation does not necessarily reflect excess demand in all or several markets, but may be the outcome of a conflict over income distribution. This interpretation of inflation fits well into a theoretical framework in which employment and output essentially depend on aggregate demand, not only in the short but also in the long run, and income distribution can be altered by bargaining, without direct consequences for the level of employment or the efficiency of the system.[3] It is a framework largely shared by several strands in heterodox and post-Keynesian economics.

In the conflict interpretation of inflation, unemployment may affect nominal wage and price inflation as a result of its influence on the bargaining position of the parties – actually, this may be regarded as a quite straightforward and simple explanation of the original empirical results by Phillips (Rothschild, 1993). This conflict interpretation of inflation may be compatible with the accelerationist view that a single NAIRU exists, but only under the assumption that the mark-up over costs is given (that is, by implication, that the rate of profit is also given) and cannot change as a consequence of wage bargaining, so that any change in nominal wages will be fully and rapidly translated on prices, and hence any persistent attempt to increase the real wage will lead to accelerating inflation (see Rowthorn, 1977; Stockhammer 2008). Even so, in this perspective the ‘divine coincidence’ is, in many ways, lost: the NAIRU does not necessarily reflect the maximum employment that can be attained given structural constraints, but simply represents the unemployment rate necessary to discipline the workers into accepting a real wage consistent with a given mark-up and profit rate. By contrast however, if persistent changes in income distribution can actually result from changes in bargaining relations, which in turn may be brought about by changes in the unemployment rate, then we would have no NAIRU at all.

To make things easier for those not used to such alternative views, it can be of help to express the point in terms of the usual, textbook graphical representation of the new-Keynesian model, with the bargained wage curve sloping upwards in the employment/ real wage space and a horizontal or downward sloping price curve given by

P=(W/q) (1+m)

and hence

W/P = q/(1+m)

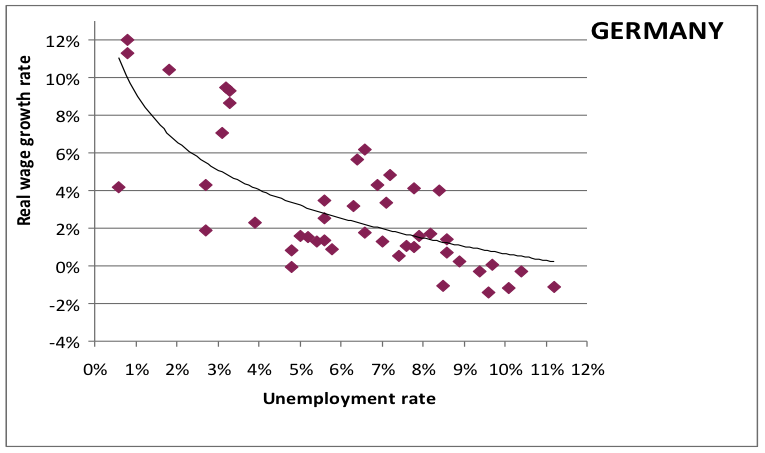

where W is the nominal wage, P is the price level, q is (marginal) product per worker and m is the mark-up over variable costs. If income distribution can be persistently affected by changing unemployment and bargaining power, as we move upwards along the wage curve, the mark-up m would fall, causing upward shifts of the price curve. In this way, no single NAIRU could be identified. The “price curve” loses its explanatory role, and the only relevant relationship is the ‘wage curve’ – interpreted as an empirical relationship between unemployment and real wages (given the institutional set-up and productivity). This is of course only part of the story – even without a mark-up, i.e. under the assumption of perfect competition, the approach would imply that the rate of return to capital can be persistently altered by bargaining relations.[4] Actually, there is empirical evidence of a relationship between unemployment rate and real wages or income shares coming from different strands of literature;[5] Figure 2 below provides a hint.

In this framework, a constant nominal wage and price inflation not only would be a symptom of distributive conflict, but may also be the means by which distribution is actually affected, if price reaction to changing wages is incomplete, and/or it takes place with a lag (Stirati, 2001; Meade, 1982, Appendix A; Modigliani and Padoa Schioppa, 1977; Tarling and Wilkinson, 1985). This in turn implies that though lower unemployment may be associated with a higher inflation rate, acceleration does not necessarily follow. The latter might indeed be the result of specific economic and institutional circumstances, such as emerged in the 1970s, among which are prolonged low unemployment, strong unions, cost push from commodity prices. The conflict interpretation of inflation also suggests that even when high inflation emerges, different routes are available to curb it. One is higher unemployment, with its economic and social costs, and reduced workers bargaining power by means of institutional changes (which has been the route followed in most industrial countries since the 1980s); the other is finding some shared solution to the distributive conflict by means of centralized bargaining and income policies affecting all incomes and not just the workers, a redistributive role of the state through progressive taxation and provision of welfare, and research and technical innovations enhancing productivity growth (in many ways, this is the route pursued for a long time in Northern Europe). Since inflation is not necessarily the result of excess demand, increasing unemployment is not the necessary therapy.

Figure 2

Data sources: Eurostat, Ameco. Real wage is hourly compensation of employees deflated by CPI, 3 years moving average of annual growth rates; Unemployment is 3 years moving average of unemployment level. Data refer to West Germany before 1991.

On the other hand, if employment depends on aggregate demand, changes in the latter, such as reductions in public expenditure, have persistent effects. (To use the term currently used in macro models, it causes hysteresis.) In fact, there are no endogenous market mechanism bringing aggregate demand back to its previous level, or in line with an independently determined potential output. On the contrary, it is potential output that in the long run will be affected by changes in aggregate demand, mainly via the influence of the latter on business investments.

Unlike in mainstream macro-models, in this framework “hysteresis” in output and employment is quite independent of rigidities in nominal or real wages or any other obstacle to competition, but is simply the way market economies normally work, even under competitive conditions. [6]

Perhaps, when inflation is caused by persistent excess demand it may tend to accelerate. But one must be aware that excess demand in labour and goods market is an elusive concept, and that potential output too may be affected by aggregate demand. There are often “reserves” potentially available in labour markets besides the unemployed (discouraged workers, involuntary part-timers; low-income self-employed, immigrants). Output therefore may be rather elastic both in the short and long run, owing to the possibility of drawing on labour reserves, and also on other factors. In the short run, changes in the intensity of utilization of labour and capital giving rise to increases in productivity are well known ever since Okun’s 1962 article (for discussion and empirical results see Basu 1996). In the longer run, empirical evidence and heterodox economic analysis suggest the dependence of aggregate business investments on changes in aggregate demand (see references in section 2 above). This brings about an adjustment of potential output to changes in demand, which is the basis for demand-led growth models currently being developed by several non-mainstream economists (Cesaratto and Mongiovi, eds, 2015; Lavoie, 2016; Levrero, Palumbo and Stirati eds, 2013; Onaran and Galanis, 2012 among others). In addition, this causes some degree of endogeneity of productivity in the long run, consistent with the Kaldor-Verdoorn empirical law (McCombie, Pugno, Soro, 2002; Ofria 2014; Yongbok and Vernengo, 2008).[7] Actually, some fairly widely accepted models of hysteresis point to the effect of recessions on capital formation as a cause of the consequent increase in the NAIRU (Rowthorn, 1995); strangely enough however there seem to be little recognition, particularly in policy making, that things may work the other way round too: positive demand shocks may cause more capital creation and hence decrease the NAIRU in the long run.

Present conditions in the European “periphery” at any rate appear very far from excess demand; price changes have a dangerous tendency to be negative, output has fallen, and though this has already brought about considerable destruction of productive capacity, it seems hard to believe that increases in aggregate demand and employment could not be met by a higher utilisation of the existing capital stock and labour supply, without generating accelerating inflation. On the contrary, evidence suggests they are the only appropriate cure for high unemployment and the dangerous tendency to price deflation.

Footnotes

- * [email protected]; I thank Walter Paternesi for assistance, Antonella Palumbo, Riccardo Pariboni and Franklin Serrano for advice and references, and Orsola Costantini and the Institute for New Economic Thinking.

- [1] In turn, this reinterpretation of the Phillips Curve as a cyclical phenomenon involved a number of difficulties in reconciling the theory with empirical evidence concerning the co-movements of employment and real wages, which cannot be dealt with here, but see Stirati, 2015.

- [2] For a critical assessment and literature review concerning empirical estimates of the NAIRU and their use in policy making see Palumbo, 2015.

- [3] See Stirati (2001) and Serrano (2006) for an interpretation of inflation and hysteresis according to these lines. Advanced expositions of the analytical background can be found in Kurz and Salvadori, 1995; Petri, 2004; important seminal contributions are in Eatwell and Milgate (eds, 1983). Surveys of the general approach can be found in Aspromourgos 2004 and 2013.

- [4] Clearly, in the background there is a different theory of income distribution and employment than in the mainstream; namely, there is no role for decreasing factor demand curves (see references in note 2)

- [5] There is an empirical literature showing that unemployment rates can persistently affect income distribution: research on the “wage curve” initiated by Blanchflower and Oswald, 1994, evidence on a “real wage Phillips Curve” (Newell and Simons, 1986), work by Shaikh (2013a; 2013b) on the US; Levrero and Stirati 2006 and Stirati, 2011 on Italy and other European countries. Concerning the short-run, pro-cyclical real wages are a well-established regularity (see Stirati, 2015)

- [6] See the literature quoted in note 2. Ultimately, the absence of endogenous mechanisms establishing the tendency of the economy to return to some natural equilibrium rests on criticisms of the analytical foundations of factor demand curves, from which comes a different view of the working of market economies, even under the assumption of free competition in all markets.

- [7] Higher investments entail that a larger share of the capital stock consists of new equipment, which embodies the latest, most advanced technology.

References

- Aspromourgos T. (2004) “Sraffian research programmes and unorthodox economics,” Review of Political Economy, Taylor & Francis Journals, vol. 16(2), pp. 179-206.

- Aspromourgos T. (2013) Sraffa’s system in relation to some main currents in unorthodox economics, in Levrero E.S., Palumbo A. and Stirati A. (eds, 2013) Sraffa and the reconstruction of economic theory, vol 1: Sraffa’s legacy: interpretations and historical perspectives, Basingstoke: Palgrave-Macmillan.

- Baker D., Glyn A., Howell D., Schmitt J. (2005), Labour Market Institutions and Unemployment: Assessment of the Cross-Country Evidence, in Howell (ed) Fighting Unemployment. The Limits of Free Market Orthodoxy, Oxford University Press, Oxford.

- Ball L. (2015) Comment on ‘Inflation and activity’ by Olivier Blanchard, Eugenio Cerutti and Lawrence Summers, ECB forum on Central Banking, May, pp 47-52.

- Basu D. (1996) Procyclical productivity: increasing returns or cyclical utilization? Quarterly Journal of Economics, vol 111, August, pp 719-751.

- Blanchard O. (1986) Investment, output and the cost of capital: a comment, Brookings papers on Economic Activity no. 1, pp 153-58.

- Blanchard O. and Leigh D. (2013) Growth Forecast Errors and Fiscal Multipliers, IMF working paper, 13/1.

- Blanchard O. (2016) The US Phillips Curve: back to the 1960s? Policy brief, Peterson Institute for International economics, no. PB16-1, January.

- Blanchard O., Cerutti, E., Summers (2015) L. Inflation and Activity – Two Explorations and their monetary policy implications, IMF working paper, WP/15/230, November.

- Blanchflower D.G. and Oswald J. (1994) The Wage Curve, Cambridge and London: MIT Press.

- Cesaratto S. and Mongiovi G. (2015, eds) A symposium on Demand-led growth, Review of Political Economy, April and July.

- Chirinko R.S. (1993) Business fixed investment spending: modelling strategies, empirical results and policy implications, Journal of Economic Literature, 31 (4) pp 1875-1911.

- European Commission (2013) Labour Market Developments in Europe.

- Eatwell J. and Milgate M. (eds, 1983) Keynes’s Economics and the Theory of Value and Distribution, London and New York: Duckworth and Oxford University Press.

- Fiebiger, B. (2014): Semi-autonomous household expenditures as the causa causans of post-war U.S. business cycles: the stability and instability of Luxemburg-type external markets, working paper.

- Ford R. and Poret P. (1990) Business Investments in OECD Economies: Recent performance and some Implications for Policy, OECD Economic department Working papers, no. 88.

- Girardi D. and Pariboni R. (2015) Autonomous demand and economic growth: some empirical evidence, Centro Sraffa Working Papers, no 13, October.

- Guichard, S. and E. Rusticelli (2010), “Assessing the Impact of the Financial Crisis on Structural Unemployment in OECD Countries”, OECD Economics Department Working Papers, No. 767, OECD Publishing. http://dx.doi.org/10.1787/5kmftp8khfjg-en

- Hillinger C. (2005) Evidence and ideology in macroeconomics: the case of investment cycles, Social Sciences Research network, march, at: http://papers.ssrn.com/sol3/papers.cfm?abstract_id…

- Khotari S.P., Lewellen J. And Warner J.B. (2014) The Behaviour of Aggregate Corporate Investment, MIT Sloan School Working Paper 5112-14.

- Kurz H. and Salvadori N. (1995) Theory of Production, Cambridge: Cambridge University Press.

- Lavoie M. (2016) Converge towards the normal rate of capacity utilization in neo-kaleckian models: the role of non-capacity creating autonomous expenditures Metroeconomica 67:1 (2016) pp 172–201

- Levrero E.S. and Stirati A. (2006) The influence of unemployment, productivity and institutions on real wage trends: the case of Italy 1970-2000, in Hein E., Heise A. and Truger A. (eds) Wages, Employment, Distribution and Growth – International perspectives, Palgrave-Macmillan, pp. 93-116.

- Levrero E.S., Palumbo A. and Stirati A. (eds, 2013) Sraffa and the reconstruction of economic theory, vol 2: Aggregate demand, policy analysis and growth, Basingstoke: Palgrave- Macmillan.

- McCombie, J.S.L., Pugno M. and Soro B. (2002) Productivity growth and Economic Performance: Essays in Verdoorn’s law, New York: Palgrave Macmillan.

- Meade J. E. (1982) Essays in wage fixing, London: Allen and Unwin.

- Millemaci E. and Ofria F. (2014). “Kaldor-Verdoorn’s law and increasing returns to scale: A comparison across developed countries,” Journal of Economic Studies, Emerald Group Publishing, vol. 41(1), pages 140 - 162, January.

- Modigliani F. and Padoa-Schioppa T. (1977) La Politica Economica in una Economia con i Salari Indicizzati al 100% e più, Moneta e Credito, no 117, pp 3-53.

- Onaran, O. and Galanis, G. (2012) Is aggregate demand wage-led or profit-led: national and

- global effects, working paper no. 40, Conditions of Work and Employment Series,

- International Labour Office. Available at: http://www.ilo.org/travail/whatwedo/publications/

- WCMS_192121/lang–en/index.htm

- Petri F. (2004) General Equilibrium, Capital and Macroeconomics, Cheltenham and Northampton: E. Elgar.

- Pichelmann K. and Schuh A. U. (1997) The NAIRU Concept: a few remarks, Oecd Economic Department Working Papers no. 178, OCDE/GD(97)89.

- Rothschild K. W. (1993) The Phillips Curve and All That, in Rothschild (ed) Employment, Wages and Income Distribution, London: Routledge, pp. 125-61.

- Rowthorn R. (1977) Conflict, Inflation and Money, Cambridge Journal of Economics, vol 1, pp 215-239.

- Rowthorm R. (1995) Capital formation and unemployment, Oxford review of economic policy, vol 7, pp 26-39.

- Schoder, C. (2014): Effective demand, exogenous normal utilization and endogenous capacity in the long run: evidence from a cointegrated vector autoregression analysis for the

- USA, Metroeconomica, 65 (2), pp. 298–320.

- Shaikh A. (2013) Wages, unemployment and social structure: a new Phillips Curve, G. & L. E. R., Vol. 17 No. 2.

- Shaikh, A. (2013) A New Phillips Curve: Wages, Productivity and Unemployment in the US, 1947-2012, paper presented at “Centro di ricerche e documentazioni Piero Sraffa”, 29.11.2013.

- Sharpe S. A. and Suarez G.A. (2014) The insensitivity of investment to interest rates: Evidence from a survey of CFOs, staff working papers in the Finance and Economics Discussion Series (FEDS), 2014-02, Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.C.

- Serrano F. (2006) Mind the Gap: Hysteresis, Inflation Dynamics and the Sraffian Supermultiplier, at: http://www.ie.ufrj.br/datacenterie/pdfs/download/t…

- Stirati A. (2001) Inflation, Unemployment and Hysteresis: an alternative view, Review of Political Economy, 13 (4).

- Stirati A. (2011) Changes in Functional Income Distribution in Italy and Europe, in Brancaccio E. and G. Fontana (eds) The Global Economic Crisis - New perspectives on the critique of economic theory and policy, Routledge, London.

- Stirati A. (2015) Real wages in the business cycle and the theory of income distribution: an unresolved conflict between theory and facts in mainstream macroeconomics, Cambridge Journal of Economics advance access 23 Feb.

- Stockhammer E. (2008) “Is The NAIRU Theory A Monetarist, New Keynesian, Post Keynesian Or Marxist Theory?,” Metroeconomica, Wiley Blackwell, vol. 59(3), pp 479-510.

- Stockhammer E., Hein E. and Lucas G., 2011. “Globalization and the effects of changes in functional income distribution on aggregate demand in Germany,” International Review of Applied Economics, Taylor & Francis Journals, vol. 25(1), pages 1-23.

- Tarling R. and Wilkinson F. (1985) Mark-up pricing, inflation and distributional shares: a note, Cambridge Journal of Economics, vol 9, pp. 179 -185.

- Yardeni E., Johnson D., Quintana M., (2016) Money & Credit: Private Sector Lending by Eurozone MFIs, Yardeni Research, Inc., February.

- Yongbok J. and Vernengo M. (2008) Puzzles, Paradoxes, and Regularities: Cyclical and Structural Productivity in the United States (1950–2005) Review of Radical Political Economics, Summer, vol. 40 no. 3, pp. 237-243.

- Wen, Y. (2007) Granger causality and equilibrium business cycle theory, Federal Reserve

- Bank of St. Louis Review, May–June, pp. 195–205.