I won’t try to call the peak. What’s more useful is to try to understand all of the moving parts, and a money view of the problem lets us do exactly that.

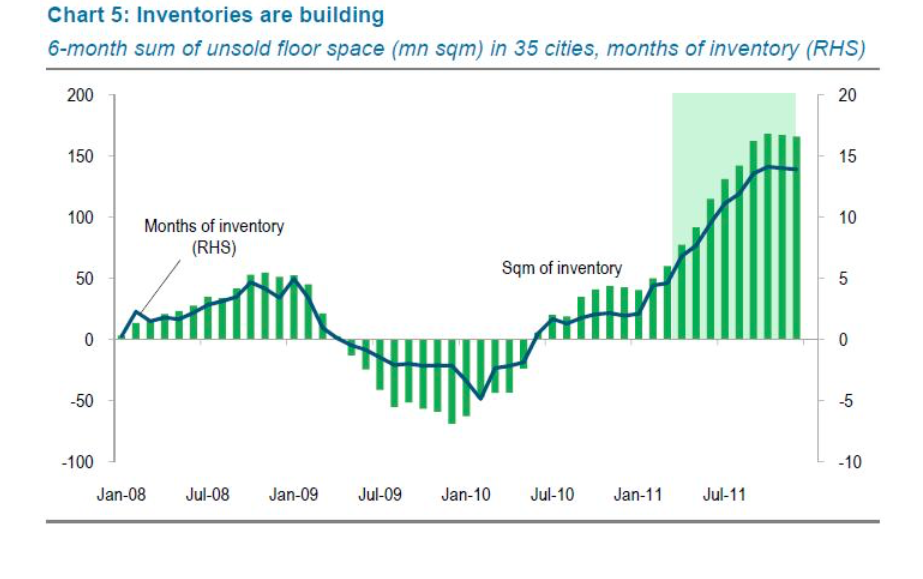

Start with the symptoms. The FT informs us that the property market is failing to clear in Hainan: sellers offering no-questions-asked refunds just to try to lure potential buyers; a moribund secondary market. Inventories are starting to pile up.

Source: CREIS, Standard Chartered Research, via FT Alphaville

Who is holding this unsold property as an asset, and how are they financing it? Mostly developers, who finance with loans. These come from banks, or increasingly, as Victor Shih points out, from private underground banks.

To stem inflation, the PBoC has been raising reserve requirements on regular banks. Higher reserves means banks can lend less out on a given deposit base. Credit is already contracting to small and medium enterprises, leading to a cash crunch. Since the reserve requirements don’t affect underground banks, borrowers will draw on them as credit tighens elsewhere. But underground banks have limits too, and they will either raise borrowing rates or deny credit as demand for loans increases.

What happens when developers can no longer roll over their financing? They are in a long squeeze, and have to sell. Property prices are already falling, and buyers becoming scarcer. A wave of inventory will have to be sold to pay off borrowing, pushing prices down further and exacerbating the underlying problem (developers’ insolvency).

To the extent that banks have to write down losses on these loans, other credit may contract as well. The central government just took 2T–3T yuan renminbi of loans to local governent finance vehicles (LGFVs) off of banks’ balance sheets. These loans finance infrastructure and other local projects. Patrick Chovanec estimates that there are plenty more bad loans where those came from. If credit is choked off to such projects, it will clearly restrain GDP growth.

Where does this end? Someone has to write down losses on these loans. If the central government buys them up and eventually writes them off, that’s the taxpayer. If the banks are forced to do it, they will need to be recapitalized, perhaps via negative real interest rates on deposits, which is just a tax on depositors, as Michael Pettis has repeatedly emphasized.

In the meantime, a collapsing property market will be devastating for China’s local governments, who have come to rely on land sales to fund current expenditures.

There’s not enough detail here to make a real prediction of the timing or of the scale of the problem, and it would be unwise to underestimate the central government’s willingness to take on private and local-government debts in the interest of keeping growth high and inflation low, which could delay the unwinding of the bubble for some time yet. What cannot be denied is that property is tied tightly into the financial system and the rest of the economy, and that when the correction comes, the effects will be far-reaching.