The BIS recently reminded us to look at gross flows, which I think is good advice. Just so, the blue line shows increases in US liabilities1 to the rest of the world, the green line increases in US financial assets abroad. The red line is the difference between them, plus a (sometimes considerable) statistical discrepancy.

A few observations.

The current account deficit is two things, as a matter of accounting. First, as I have shown it in this graph, it is the net increase in US liabilities abroad. Second, it is (roughly) the trade deficit, exports from the US less imports to the US. The two must be equal, since every good or service bought abroad must be paid for abroad. The international dollars needed to make payment can be acquired either by selling an export or by borrowing them abroad.

As the graph shows, however, the relatively stable current-account balance can conceal wild fluctuations in the corresponding gross financial flows since the onset of the financial crisis in 2007. Plenty of borrowing and lending, that is, goes on without a direct connection to trade flows, and this is why the gross flows are important.

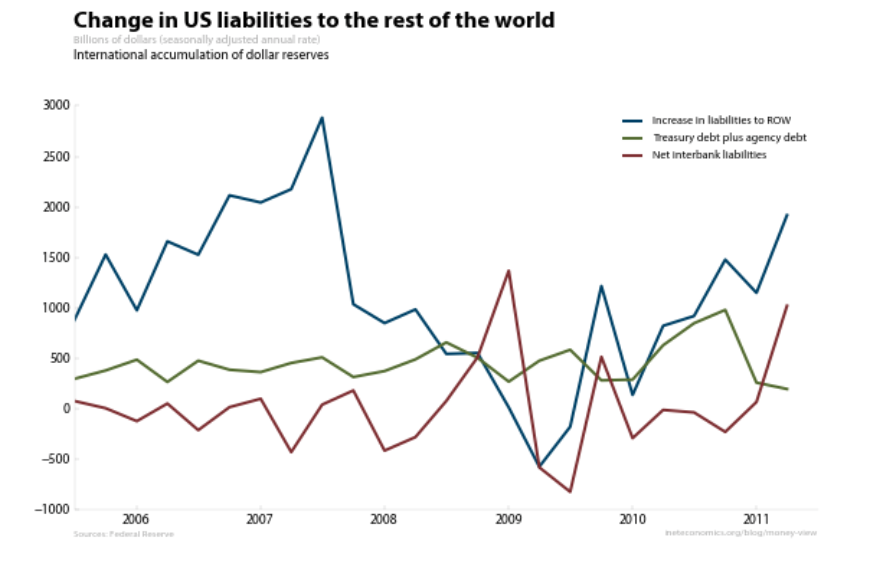

Kindleberger’s collection of essays International Money has been on my desk for a few weeks. He likes to think of the US as a bank, its liabilities serving as liquid assets for the rest of the world. The next graph shows the US liabilities line from above, along with two of its components.

The blue line is the same as the blue line in the first above. The green line shows the world’s accumulation of Treasury debt. This was going strong for much of 2010, but QE2 slowed it down by the end of the year and into 2011. The red line shows what happened as a result: the rest of the world sold its Treasuries to the Fed and deposited them in US banks. The world accumulated deposits instead of government debt.

One way to read all of this is that the US continues to provide the world’s reserve assets. Notwithstanding China’s grumblings about reserve diversification, the S&P downgrade, and the absence of any particularly good economic news, US liabilities are still what the world wants to hold.

Next time, I’ll look at the asset side of the ledger and complete the picture.

1 Note that all of this data is from the Flow of Funds accounts, table F.107, where the accounts are presented from the point of view of the rest of the world. So their assets are my liabilities and vice versa.