An interview with Thomas Ferguson on the 2024 US election conducted by Andrew Yamakawa Elrod and Tim Barker for Phenomenal World

First published at: Phenomenal World

As the nation prepares for a second Trump administration, the mood among many Democratic Party officials has been one of bafflement and astonishment. How could voters have failed to rise to the defense of the democracy and “institutions” that Democrats spent eight years lionizing as bulwarks against an incipient Republican Party fascism?

Among the electorate, however, disappointment is just as likely to be at the choices on offer as at the outcome itself. The Pew Research Center in exit polling found 64 percent of respondents thought the campaign “was not focused on important policy debates.” In pre-election polling, it found 63 percent of Trump supporters and 62 percent of Harris supporters sharing such sentiments.[1] Given how diminished the scope for change appeared to most voters, it is perhaps unsurprising that turnout fell by 2.6 million voters below the level of 2020—while the voting-eligible population increased by 3.5 million—with those staying home concentrated among large cities in swing states: traditionally Democratic-voting precincts.

What explains the American party system’s continued rightward drift? On this question few analysts have offered insights as trenchant and consistently significant as Thomas Ferguson, currently Director of Research at the Institute for New Economic Thinking. For the past four decades, he has argued that American politics is best explained by an “investment theory of politics.” According to that theory, electoral outcomes are shaped by competition between the parties not over the preferences of voters—as argued by the “median voter theorem” popularized by postwar social science—but rather by a different set of preferences altogether: that of donors.

Countless surveys show that voters preoccupied with life and work are uninformed when it comes to the finer points of foreign trade; the federal budget; or the determinants of investment, unemployment, and inflation. If they must select among candidates and platforms decided elsewhere, how are those choices defined? To either the chagrin or inspiration of many historians, economists, and political scientists, Ferguson has spent decades in campaign finance records and the historical archives of key twentieth-century business and party leaders.[2] The evidence he’s found demonstrates that the complex of business corporations and their financiers—whose growth plans would be made or broken by changes to tax law, regulation, foreign policy, and exchange rates—significantly shape candidate nominations, electoral campaigns, and the careers of politicians. In a money-driven campaign and media system, these are the contributions that matter most.

Despite the revelatory nature of his archival findings to the theory of how electoral realignments happen, Ferguson’s prescient warnings of the deep decay of American party politics appeared to go unheaded by partisans ostensibly alarmed by the state of American democracy. As readers search for answers about how to interpret the 2024 US elections, Phenomenal World editors Tim Barker and Andrew Elrod reached out to Ferguson for a conversation about his thoughts on the recent campaigns. It has been edited for length and clarity.[3]

An interview with Thomas Ferguson

Andrew Elrod: One thing that struck me about the 2024 election, and really about Democratic strategy since the 2022 midterms, was the degree to which the party seemed to be engineering a demobilizing operation.

Thomas Ferguson: Let’s put it in very simple English. Joe Biden was the consensus candidate of the Democratic Party establishment in 2020 because he was the only one who was broadly acceptable within the Party, looked viable against Trump, and could hold off Sanders. His candidacy was strongly reminiscent of Paul von Hindenburg’s second run for president in the last days of the Weimar Republic, when everyone from liberal elements of big business to the Social Democrats united around the doddering octogenarian as the only candidate capable of defeating Hitler.

I like to start the discussion of recent American politics with the 2014 midterm elections, which I analyzed in a piece with Walter Dean Burnham. The big story in 2014 was the stupendous decline in voting turnout compared to the presidential election in 2012. The turnout drop off was the second largest ever in percentage terms. Only the 1942 decline was greater, because millions of voters were shipping out across the globe to serve in World War II. But in many states turnout in 2014 collapsed to astonishingly low levels, akin to those of the Federalist era (when property suffrage laws limited voting). Regional differences in turnout between the North and the South also pretty much closed up for the first time since perhaps 1872, when much of the former Confederacy was still under occupation by Union armies. But this wasn’t because Southern turnout arced upward. Of course voter turnout in the South had been slowly rising since the civil rights revolution of the 1960s, but what finally brought the regions to parity in 2014 was plunging northern and western turnout. California probably witnessed the lowest rates of voting since it came into the Republic, while Nevada, Utah, and other states hit true lows. Burnham and I concluded that this signaled voters were sick of the establishments of both parties—that real upheaval impended.

What we got were challenges from outside the normal political spectrum. Trump challenged from the right, Sanders from the left. The dramatic entrance of candidates who did not stand for business as usual started a process in which turnouts rose sharply with these outsiders pulling in lots of people on both sides.

In 2016, Hillary Clinton and the Democratic Party leadership would not deal with Sanders. They famously cut the Sanders movement out of everything. In 2020, with Trump in the White House, Sanders ran again and lost, but he did quite well and the rest of the party consolidated around Biden. Sanders was undeniably a major force in the party and his movement could not be ignored. Elizabeth Warren represented a somewhat similar force.

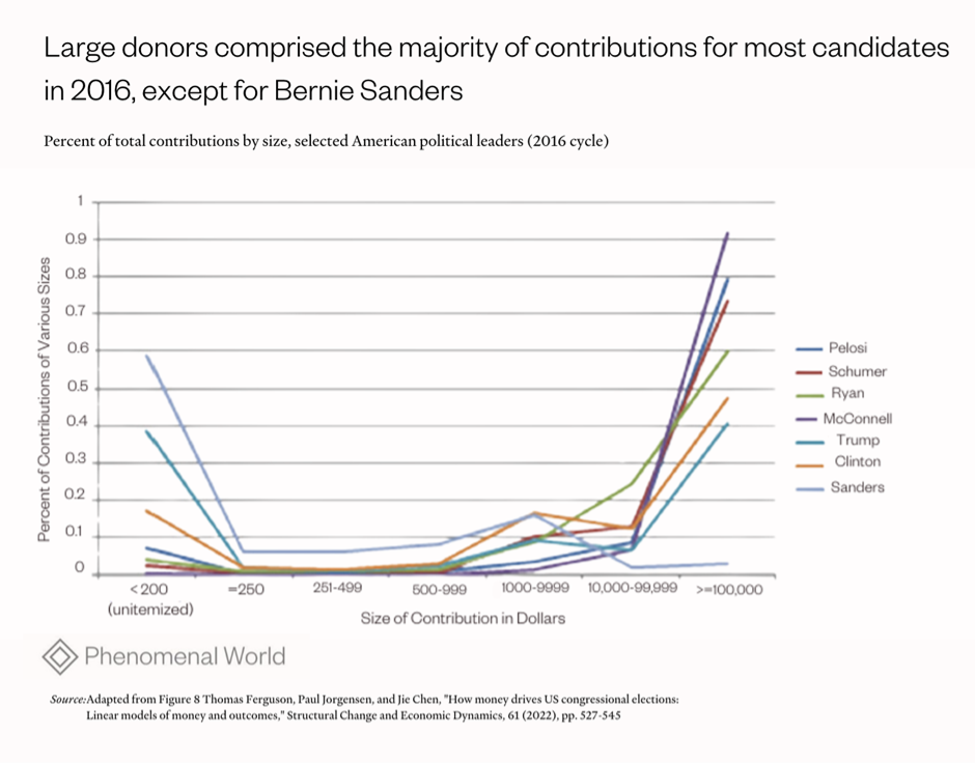

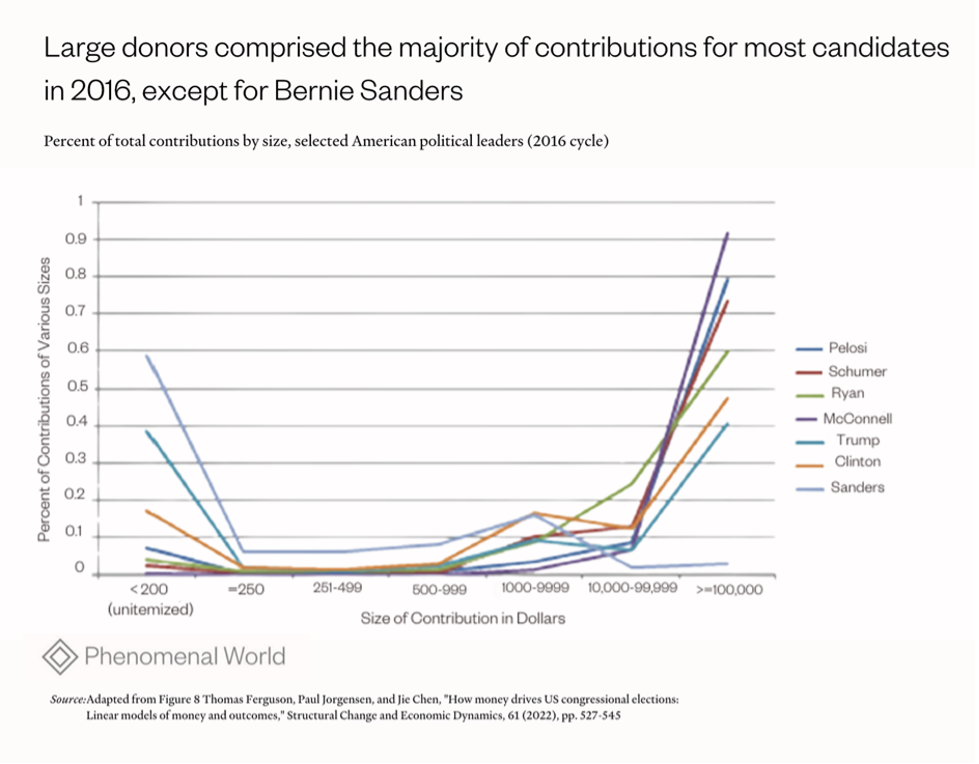

In contrast to 2016, Biden let Sanders and his movement into the campaign and then into a kind of power-sharing arrangement. Underneath all the discussion of investment approaches to politics that I’ve done is a basic model of American electoral politics in which elite conflict driven by industrial structure interacts with broader social conflicts. What was happening after 2014 was the political expression of people who were definitely not super rich in any way, shape, or form. You can see that very graphically in the paper that Paul Jorgensen, Jie Chen, and I did, where we show the percentages of cash coming from various size levels of contributors. There’s basically one guy who’s not getting any money from the super rich: Sanders. All the other candidates are. Trump has that peculiar barbell shape: he gets a lot of small money, but he gets enormous amounts of big money, too.

Biden thus came to power in 2021 in coalition with a serious, articulate progressive agenda. The bulk of the Democratic party didn’t like that: Pelosi and, for that matter, most of the Biden people were not wild about the Green New Deal. But Democrats knew they had made a big mistake in 2009, when they came in and did the small stimulus. Everybody agreed they could not repeat that disaster. Even the financial community took the point—emblematic of this is a January 2021 paper by Robert Rubin, Peter Orszag, and Joseph Stiglitz. Basically, it says you need to go big on fiscal policy.

But the understanding of the financial wing of the party was that this would be a temporary stimulus. I’m not saying this worked out because three guys agreed. The agreement reflected a current of thinking that was very strong—Rubin’s signature in particular is representative of that. The guiding idea was “let’s go big early and then taper it back.”

The result was a consensus to try to put a big package through. And that happened: the American Rescue Plan, which the Wall Street Journal just the other week was denouncing quite mistakenly as the cause of inflation. At that point, Biden’s popularity was very high. But the program was rapidly cut back. To caricature this for clarity: for about two years, you had almost a European social welfare state briefly in the United States. You got all kinds of things that you should have—the stimulus allowed people to pay for doctor visits, cover essentials, and there was meaningful childcare assistance—and then suddenly you didn’t again. Nearly all of that was rolled back before the 2022 election. Not quite all of it, but most of it. And the administration pretty much gave up on Covid-19 and declared victory prematurely, as Phillip Alvelda, who led the DARPA project that helped develop the mRNA vaccine, has spelled out in damning detail.

AE: Let’s talk about the Inflation Reduction Act—the culmination of these struggles in Washington that opened with the American Rescue Plan and intensified as inflation accelerated.

TF: The killer problem for the climate politics part of the Biden agenda, in my opinion, occurred after the war had started in the Ukraine. The Russian invasion drove oil and liquefied natural gas prices to the moon. Suddenly liquefied natural gas (LNG) exports from the US looked really crucial to supplying the rest of the world. Large fossil fuel interests saw their opportunity and went on the offensive. You could see this as it was happening. The new view in the US foreign policy establishment was, “you know what? Domestic fossil fuel production is a great weapon in foreign policy. We can supply Europe with the energy they’re losing as we finance the war with Russia; in fact we can supply many parts of the world. Let’s not push out the natural gas or oil guys too fast.” And the Biden administration discovered you can garner campaign contributions from those folks. As we know, US drilling increased, not decreased under Biden.

AE: You’re arguing that the rescue of the various green energy tax credits from the whole Build Back Better agenda in the spring of 2022—the green capital push—was also a way to give fossil fuel producers a stake in the Bidenomics coalition?

TF: That’s exactly what happened, though the Democrats were never going to be as hospitable to oil and gas as the GOP, since they also represent the possibility of action on climate change. The key point is that oil and LNG forces were no longer being treated as pariahs anymore, but as a potentially important international economic resource for the United States, a view that was shared widely within big businesses and the foreign policy establishment. I’m only repeating judgements that are obvious in, for example, Jamie Dimon’s “Letter to Shareholders” in the J.P. Morgan Chase annual report.

AE: How does the problem of inflation enter the political calculus here?

TF: The inflation was principally a supply-side story. Covid-19 happens. You can’t get anything or go anywhere. There’s nobody able to work in many places. You’ve got hundreds of ships sitting off ports that can’t land. Almost everything grinds to a halt. It has nothing whatsoever to do with any government spending. When Servaas Storm and I worked through the spending statistics very carefully in the first of three papers we wrote on this, we showed that, in fact, the federal spending had trickled off to almost nothing by October 2021, while inflation went higher and higher, surging principally in response to the Ukraine war, but also to problems related to climate: droughts, wildfires, and intense storms hitting crop patterns and infrastructure. These interact with oil prices which also drive up food prices. That last point is shown beautifully in a separate paper by Carlotta Bremen and Servaas Storm.

In my opinion, the Biden people should have moved to quickly choke off general financial speculation in commodities. Not everyone agrees with me, but I think they could have done it. A former Commodities Future Trading Commissioner actually told me he thinks US regulators probably could have acted, though we agreed that coordination with the Europeans would have been much better. The administration could have at least made the point and asked Congress for the authority to do something.

If the authorities had gone back to the older, pre-deregulation rules where end users and producers of the product were the folks mostly allowed into these markets, you would have contained those big price spikes, and the stabilization would have spilled over onto food prices.

AE: Can you say more about how the regulation of commodity futures contributed to inflation?

TF: In the old, pre-deregulation days, you couldn’t get into those markets on the financial side, except with very severe limits. You had to be somebody who actually used the commodities in their products, or you had to be a primary producer trying to hedge. The Bush-era regulatory changes made a huge difference. You may remember when AIG went bust in September 2008 and Tim Geithner, Hank Paulson, and Ben Bernanke got the federal government to rescue it. The team administering AIG had to get rid of a huge pile of commodities. They sold it all off one afternoon. It was shocking. AIG had all kinds of things in there: crops, metals, you name it. World commodities took a hit. But what that showed is how much financial firms just go in and speculate in this stuff. This is a US, a European, and, indeed, a world problem.

But Biden’s top economic policymakers, in the National Economic Council and elsewhere, drew heavily from hedge funds, private equity, and other financial types—despite talk about all the labor people in the administration. They should have done something. They should also have moved much more vigorously on antitrust. This is partly the responsibility of the FTC, where Lina Khan was certainly willing, but she was just getting into the job and met with huge internal resistance. They could have put a lot more emphasis on antitrust earlier. They didn’t. The antitrust section of the Justice Department could also have moved much faster than it did. Now, the Biden antitrust record overall is pretty good, but they were slow when it really mattered, at the start of the inflation, with the reopening of the freight system. They should have jumped in with something like a World War II-type coordination system—to open those ports much faster.

Tim Barker: Why was it that Biden was so relatively good on antitrust? How do we explain Lina Kahn?

TF: That pick reflected, first of all, the Warren and Sanders wings of the party. That was the appointment that signaled to everybody instantly that they were going to be serious about this. There is also, though, a strong minority view even in Silicon Valley itself that the smaller startups are bled by the platform companies. You can see that today in the Vance wing of the Republican Party.

But unfortunately, the Biden people dragged their feet. They should have controlled “greedflation” and paid more attention earlier to algorithmic pricing. It’s crazy to me how many economists even from the left kept denying “greedflation.” It’s clear in the data.

The administration’s slow response to inflation turned into an ostrich policy. In 2024, this was politically disastrous. They just kept proclaiming themselves as the most labor friendly administration. Sometimes they said in history or sometimes since FDR. There were all these folks, David Autor, Paul Krugman, and Arindrajit Dube saying that real wages were rising. Servaas Storm and I have written three very detailed papers on this, and we have walked through the evidence, and we conclude that no, in general, wages were not rising. The very lowest wages rose a tiny amount, pretty plainly a response to much greater workplace hazards, and everybody else’s wages lagged behind inflation.

Even within the wage data, there’s something of an optical illusion: Hourly wages rise, but working hours are dropping a lot. Average weekly real earnings are falling. No matter how you do it, most people are not keeping pace. As of our most recent paper, the overall loss is about 3 percent. Now the numbers in real wages were getting better over the course of 2024, and so that number might change slightly, though not by much. The fact is as we said, inflation’s decline without a recession came mainly from restored supply chains, some delayed expansion on the supply side, and a loss of widely distributed purchasing power—a fall in American real wages.

What was happening to people’s wages and incomes would have been much clearer if analysts would have stopped confusing people with statistics about hourly wages and simply focused on household median real income, where the numbers have been obviously disastrous if very slow in coming.

Almost everybody knew this, intuitively, when they went into a food store to buy anything at all. For the Democrats to keep parroting their “we’re the most pro-worker administration ever” line in 2024 was suicidal, even if their appointments to the National Labor Relations Board were truly labor friendly and had key impacts on specific campaigns. All the numbers for 2024 are not yet in, but the net change in the percentage of the workforce unionized during the entire Biden presidency is going to be either zero or very close to that.

In the election debates, it did not help that Democratic economists kept ignoring the actual record of the first Trump administration. Trump sharply criticized the Fed for prematurely hiking interest rates. Wages barely rose during his first term—leading to increasing doubts about the Phillips curve—but working hours went way up. Accordingly, the median household income figures rose a lot. Democratic economists were not wrong to note that the tax code and deregulation measures tilted heavily in favor of the rich, but many just ignored the short-run income rises that benefitted everyone, including minority groups, substantially. The number of pages in the media over the last two years pushing weird theories about why people didn’t appreciate that they’d never had it so good was a vast diversion.

TB: Some people recognized the “greedflation” problem. LAEl Brainard was one of the most outspoken about this, and the administration even tried to do a little jawboning.

TF: When Brainard was still on the Fed board, she was often the most reasonable person in the published meeting minutes. Voters had a much better understanding of these issues than the media discussion. The truth is that while you have many Democrats saying people are stupid, it was the elites that were stupid. It’s really a case of that saying: You can fool all the people some of the time, and some of the people all of the time, but you can’t fool all the people all of the time. The Democratic campaign found that out. Telling everyone that American democracy itself will end if you don’t vote them back into power after you’ve steadily lost purchasing power on their watch was just not going to cut it.

AE: Was there any contingency at all in 2024? Some argue that no matter what campaign the Democrats ran, they would have lost. The outcome was overdetermined—not because of the administration’s conservatism, but because inflation was global and so was the anti-incumbent wave of elections.

Others say that the Harris-Walz people actively ran a conservative campaign that failed to differentiate from the incumbent, and repudiated key parts of their base, very openly, intransigently, and as a result they were punished at the polls. Do you side with one or the other of those explanations?

TF: People knew their real earnings were declining. That was, in my opinion, fatal in the absence of a more dramatic break with Biden. The inflation situation defined the “Macroeconomics of the Second Coming” of Trump. What was crazy is the resistance in the media, the New York Times, the Washington Post, and elsewhere to this rather obvious point. I spoke with various economics writers in some of those publications, who had some idea of what was happening, but they were afraid to touch it. People talk about the fragmented media context—what we really have is media balkanization with overarching partisan divisions, and almost everybody, including bloggers, takes their cues either from some party or party-related apparatus. Critical assessments of the wage data just did not get published. Ditto for the closely related issue that we kept documenting: that wealth effects from the Fed’s quantitative easing were also a major factor in driving inflation on, too. Only now are the Fed and the IMF publishing studies that recognize this.

But Harris and Walz did not break with Biden, not even respectfully, not even implicitly. Instead, they told everyone to be joyful. They were extrapolating from the outpouring of joy when Biden finally pulled out, which was real, but then they failed to articulate anything different, except an empty emphasis on “opportunity.” Let’s forget the campaign’s ridiculous appeal to crypto as an opportunity for black males—the whole package was fairly vacuous and it went over like a lead balloon with real people almost regardless of race or ethnicity.

I do think there were ways the Democrats could have won the election. Their situation was rather like Truman’s in 1948, when he had presided over high inflation and was down in the polls. He solved that problem with an assist from a major oil company that came up with money for the famous “whistle stop” train campaign that took him around the country to meet with Americans. Now, he didn’t repudiate himself—he ran against the “do nothing” Republicans in Congress and narrowly won. Biden’s Hindenburg strategy, of course, made that kind of strategy difficult, since it was premised on pulling in as much of big business as possible against Trump and attracting as many big donors as possible—including Republicans. Harris and Walz persisted in that path, and even more aggressively courted elusive moderate Republicans, but they could have drawn much clearer lines on Social Security, which they barely mentioned, medical care and public health, or even—imagine this—strongly defended Lina Khan and her impact on Americans instead of parading around with her critics. The campaign could have simply said it would fix the problems already identified in Congressional hearings with health care companies denying medical coverage to policyholders. People are desperate and very angry, as the murder case in Manhattan illustrates, but healthcare all but vanished from the front-page political agenda since the epoch-defining pandemic.

Instead, they talked up ideas for controlling “greedflation” in grocery prices—one sector from which they knew they could hardly hope to attract campaign contributions. I’m convinced most voters saw right through the thin proposed remedies—if they were even aware of them—but we can wait for serious post-election survey data to make sure. The campaign’s concentration on Republicans and donors who mostly wanted nothing to do with such subjects is obvious.

Political science struggles to account for the overwhelming influence of big donors on our elections. In 2016, the mainstream social scientific consensus ascribed Trump’s victory to racism and sexism, brushing aside very sharp evidence that voters did not see significant differences between the parties on other issues, and in particular the economy. Or they told us fables about how “professionals” ran the party—a theme that has reemerged this month in claims of a supposed NGO “groups”-driven leftward drift in the party—instead of major donors.

TB: In that connection, I have to ask about crypto, which is by some accounts the largest corporate sector intervening in this election, and one that seems to have a big influence operation in the media.

TF: My colleagues and I are writing a piece on crypto. When we started, we were focusing on its inroads in the Democratic Party because only one Republican in the House voted against a major piece of proposed legislation to regulate the sector. There’s no variation on that side, which gives little space to model anything, so we were very interested in which Democrats were and were not voting against the industry. But crypto is probably not the biggest sector in campaign contributions. Oil, gas, finance, and technology—the high-tech firms, too—are the much bigger story. The big numbers you see rest on amalgamating all of tech with crypto.

There are serious problems with existing coverage of political money. My colleagues and I “roll our own” data, as it were, pulling it straight in from the Federal Election Commission (FEC) ourselves and sometimes the IRS. What we find in our accounting usually differs from what journalists and many scholars claim, sometimes dramatically. In the piece we wrote on Sam Bankman-Fried and FTX, for example, we immediately found tens of millions of dollars more than other journalists were reporting at the time.

Yes, the crypto people are big. But I doubt very much that their campaign spending is unique. The real story you want to concentrate on with crypto, I think, is financial stability and transparency. Financial stability and “know your customer” rules are actually organically connected; when you don’t know what claimed assets really represent and you can’t ascertain that, you are asking for trouble. Comparisons of the huge rise in crypto recently with Tulip Mania are a bit unfair; the flowers at least had real decorative uses. No heavy hand of any government caused the crypto collapse during Covid. It is intrinsic to the phenomenon. Tech fixes that are supposed to guarantee stability in stablecoins failed; those things stay stable to the extent they have an outside guarantor. The big question is how much the banking system will become an appendage of crypto.

A lot of political money data is also still unexplored. There are vast inflows into state political machines that are not in the FEC, and can only be found in the IRS numbers. Meanwhile, the IRS has been retiring many of the reports and been very slow publishing recent ones, so it’s mostly terra incognita in need of serious research. And news outlets—the New York Times, Bloomberg, and other folks—pour lots of money into polling, but devote little attention to analyzing political contributions, beyond making lists of billionaires.

The sad fact is that even right after the reforms that came out of the 2008 financial crisis, Congress had real trouble standing up to finance interests. We know now that US Congressional elections are linear functions of money and careful tests show that that is not principally because money is following votes, but rather the reverse. You can actually watch gambling odds on the new prediction markets change as money pours in sometimes. It does not help that the leaders of neither political party want to regulate political money or their own stock transactions in any serious fashion. Or that so many of them, their aides, and their children and spouses shamelessly turn into lobbyists at the first opportunity.

AE: What does the evolving industrial structure and the investment theory of parties explain about the current political landscape? As a theory of historical explanation, your work has shown how business polarization in moments of changing industrial structure has in the past led to moments of realignment. Yet over the past four decades or so, there seems to have been a prolonged decay and failure of realignment to occur. What kind of period are we living through? Where is the industrial structure headed? Is business polarized? Why is a realignment failing every four years?

TF: I’m cautious about this, especially now because my colleagues and I are still doing the data for 2024 and I’m a believer that if you don’t have access to archival data, you can study public statements, but they’re imperfect evidence.

In the old paper that Jie Chen and I published back in 2005 in the Journal of the Historical Society on realignments we found the last New Deal election was probably 1968. At that point, we enter a new political era. We are planning to redo that paper, because time series statistics have developed a lot and there’s a lot more data. But I think it is safe to say that the period after 1968 wasn’t as Republican-dominated as is often said, since the Democrats held the Congress through into the 1990s. But I would say this: that period was pretty plainly one in which organized labor declined steadily. If you want a simple index, just take the percentage of the workforce that’s unionized and watch it, and it goes down, down, down, down. Particularly in the private sector now, it’s microscopic at about 6 percent. That’s a real realignment, I think, from the perspective of investment theory.

Today, we see that the wealth effect that resulted from the Fed’s quantitative easing policies, especially after 2020, had a major political implication. The enormous boom in financial and housing wealth accrues principally to the top income brackets. What this means is that even discounting inflation, the weight of the billionaire and near-billionaire groups has greatly increased. You just see this simply by counting billionaires who can’t qualify to make the Forbes 400. It’s remarkable: there are now almost as many billionaires who don’t qualify for the Forbes list as there are on it.

Large chunks of the economy are restructuring around this redivision of income. Politics is an integral part of that. I find reporters are increasingly comfortable writing up whatever billionaires have to say without including criticisms. For example, Kamala Harris brought a large number of billionaires into the campaign. Reid Hoffman actually said something to the effect that “I’m going to take her around and support her, but we have to get Lina Khan out of there.” What counts as acceptable behavior is changing a lot, because the safeguards that used to be in the system are gone.

Now that brings me to one of my favorite points. In my book on the investment theory of parties, Golden Rule, I had an Appendix on what I called the “black hole theorem” of the press. If you’ve got a for-profit press dominant, there’s all kinds of things they will not print, because it will hurt their owners’ interests if they do. Doesn’t matter what readers are thinking, as it won’t be profitable to attract them. Daniel Chomsky has published several excellent papers using the archival collections of publishers and editors of major papers that show how this works. But this year you could see the devastating impact of what you might call the “loss function” of excluded information from the for-profit news coming right up front. At the Washington Post and the Los Angeles Times, the owners just intervened and said “we’re not going to endorse anybody.” This is not an autocratic aberration, it stems from the development and consolidation of profit-oriented markets for information.

The consequences in the blogosphere are not edifying either. Various tabulations are around of how many so-called influencers are active that don’t fit into mainstream media, but the crucial point is that this influencer culture is permeated by a money-driven, product-selling logic. The apparent multiplication of media that’s supposed to be small and uninfluenced by money is an illusion. There’s a kind of Jacksonian-press efflorescence of outlets, but not real qualitative variety. When printing underwent technical innovations in the early nineteenth century, what you actually saw were all kinds of folks subsidizing small papers, either directly or indirectly. Larry Goodwyn made the point crystal clear in his memorable study of Populism, too. Then as now, the parties, the White House, and media elites collaborate on standard narratives which are retailed around. I use the term carefully—this is done over email and through teleconferences of influencers. They believe they’re getting inside information when in fact they are just getting the party line. As Goodwyn said, a big reason for the Populists’ relative success was that they had a press of their own.

TB: There’s almost a sort of neo-Sunbelt shift, right? Elon Musk has moved to Texas. Texas and Florida seem poised to expand even further their share of the population and the Electoral College.

TF: Fair enough, but the biggest state for data centers is Virginia. And the Northeast is not full of people clamoring to increase unionization in biotech or other high-tech enterprises.

The advent of private equity makes a big difference. They are not simply hedge funds or passive asset managers. They actively manage companies. They’re usually harshly anti-union. The spread of private equity into the rest of the industrial structure has been very marked. But that whole area of financial control of non-financial companies needs more analysis.

TB: In 2020, there was private equity money on both sides.

TF: But the big players were for Trump as my colleagues and I showed in detail. It was the same thing in 2016, and I am sure that’s going to come out in 2024 too. The really big private equity firms are mostly heavily Republican.

Look, when you don’t have the data, you don’t have the data. People who are reporting on the 2024 election now are using stuff that came out in October. End of the election stuff with the FEC has yet to appear.

What my colleagues and I find repeatedly is all kinds of people using different forms of their name and their employers. I started doing this by hand in the ‘80s and ‘90s on data that would be printed out for me and alphabetized by friendly FEC folks, all of whom have left that agency. Name variations and affiliations cause lots of problems. My favorite, one I remember clear as a bell, is a guy who claimed he had no business attachment whatsoever. He was actually the chairman of the largest health insurer in the United States. But he just listed himself as retired.

Jorgenson, Chen, and I wrote a paper on the 2012 election in which we spelled out a lot of these data problems. They have not been fixed by the FEC or others. The industry assignments are not super reliable. An antitrust lawyer told me the blunt truth, which was that the firms often don’t put the correct classification numbers down because they want to do mergers or stay out of an antitrust suit. Also lower-level folks sometimes just fill out these forms with what they reported last year.

I’ve always thought the heart of realignment was the reconfiguration of the industrial base—in other words, the people paying. When those figures change, the system changes. And they will then help reconstruct the system from the top down, just like the Texas oil guys I wrote about in the New Deal.

For realignment to occur, you need a government that really wants to restructure the system, solidify new configurations, and bring forward more radical demands. We may see that come January. You know you’re not in Kansas anymore when Dr. Oz is nominated to be in charge of Medicare.

Notes

[1] A total of 9,609 panelists responded out of 10,604 who were sampled from November 12 to November 17, 2024. https://www.pewresearch.org/wp-content/uploads/sites/20/2024/12/PP_2024.12.3_election-2024_REPORT.pdf

[2] Thomas Ferguson, Golden Rule: The Investment Theory of Party Compeition and the Logic of Money-Driven Political Systems (University of Chicago: 1995).

[3] Thomas Ferguson is Professor Emeritus at the University of Massachusetts, Boston; and Senior Fellow at Better Markets. Dr. Ferguson notes that he is not speaking on behalf of any organization with which he is affiliated.