From the perspective of innovative enterprise, we ask how Musk might abuse his power of strategic control—and what that would mean for corporate governance reform.

Elon Musk’s Voting Power at Tesla

Elon Musk is the CEO of the world’s leading electric vehicle (EV) producer, and he wants to keep it that way. As one of the world’s richest people, in large part because of his shareholdings in Tesla, one might think that Musk has nothing to worry about. That’s a delusion of which he is keenly aware. Increasingly over the past decades, corporate raiders, aka hedge-fund activists, have extracted the profits of America’s most successful companies to become ultra-rich. Musk wants to keep Tesla under his own control.

As we detail in our INET working paper, “Tesla as a Global Competitor: Strategic Control in the EV Transition,” Musk’s defense against predatory value extractors is the voting power that his shareholding in Tesla confers on him. In an X post on January 15, 2024, as the Delaware Court of Chancery was deliberating whether to rescind his massive 2018 stock-option package, Musk explained the importance of that plan to him:

The reason for no new “compensation plan” is that we are still waiting for a decision in my Delaware compensation case…I put “compensation plan” in quotes, because, from my standpoint, this is primarily about ensuring the right amount of voting influence at Tesla.

Musk claims that he needs the voting power of about 25 percent of Tesla’s outstanding shares to be “influential”, but “at 15% or lower, the for/against ratio to override me makes a takeover by dubious interests too easy.”

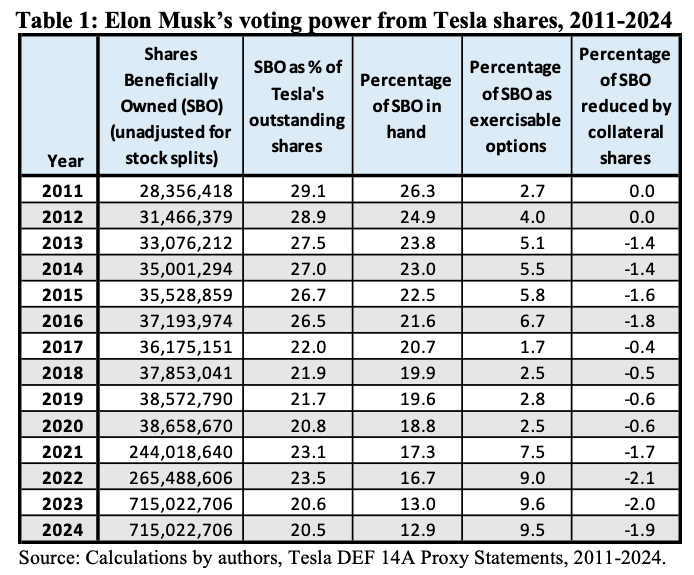

On January 30, Judge Kathaleen St. J. McCormick of the Delaware court nullified Musk’s 2018 stock-option package, worth about $50 billion (depending on the prevailing Tesla stock price). Tesla’s board, of which Musk is a member, then campaigned to convince Tesla’s shareholders to vote to reinstate the stock-option plan, securing a vote in favor at Tesla’s annual general meeting on June 13, 2024. With the 2018 stock options available to him, Musk has about 20 percent of the voting power of Tesla (see Table 1); without it, about 13 percent. Hence, the importance of the 2018 stock-option grant for Musk to remain “influential” at Tesla, capable of fending off “a takeover by dubious interests”.

Typically, a CEO would need 50.1 percent of a company’s voting shares to be unassailable by outside shareholders. So why does Musk claim that 25 percent is sufficient, while 15 percent is not? The answer stems from a change in Tesla’s company bylaws, adopted inconspicuously by amendment to its Certificate of Incorporation in December 2009 as Tesla was preparing for its initial public offering (IPO) that took place on June 29, 2010. The bylaw requires a “supermajority” vote of 66.67 percent of the company’s shares outstanding to (among other things) elect directors to the board. Directors have the legal right to hire and fire the CEO.

With Musk in possession of 20 percent of the votes, it would take 83.38 percent of the non-Musk shares outstanding to vote him out. With 13 percent of shares, the proportion drops to 76.67 percent (with a typical simple majority rule in place, the threshold would fall to 57.59 percent). Even with 25 percent of Tesla shares outstanding Musk is not invulnerable to attack, but the threshold for a non-Musk shareholder victory increases to 88.93 percent. Hence, Tesla’s supermajority bylaw permits Musk to secure his strategic control with proportionally fewer votes than one might think.

Over the course of the two decades that he has been at Tesla, with 16 years as CEO, Musk has accumulated rights to shares, and thereby votes, a) by investing $291.2 million in the company, b) through shares of SolarCity that Musk held, converted to Tesla shares when Tesla acquired it, c) by shares acquired when he exercised stock options in packages granted to him in 2009 and 2012, and d) by the vesting of stock options in the 2018 plan that remain exercisable (i.e., Musk can exercise them at any time he wants up to their expiration in January 2028).

The only time that Musk has sold any of his Tesla shares was to help finance his takeover of Twitter (renaming it X). He raised $28.7 billion by selling 110 million Tesla shares in 2021 and 2022, representing 3.5 percent of Tesla shares outstanding at the end of 2022. Musk’s shares beneficially owned (SBO) in 2024 were reportedly 715 million shares (see Table 1), but if the Delaware court enforces its recission of his 2018 stock option, his SBO would fall to 411 million shares.

Dilution of Musk’s voting power

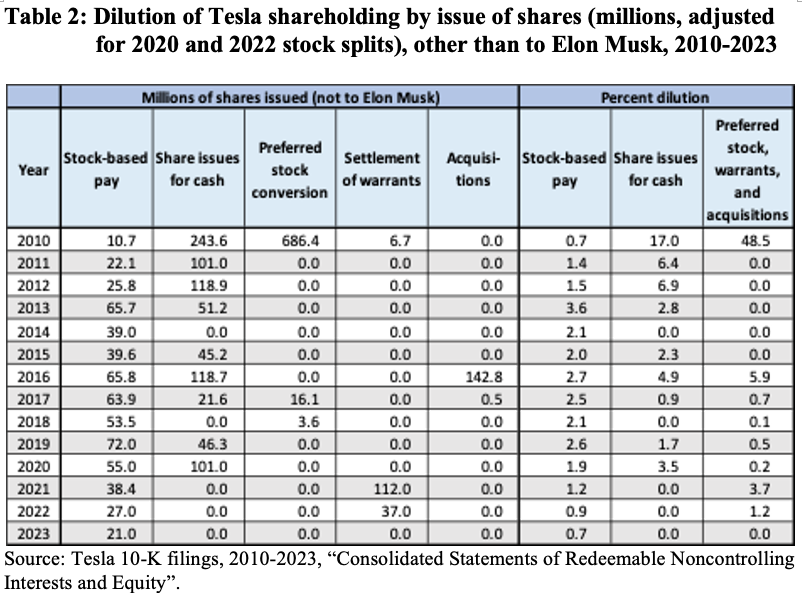

Other than the self-inflicted reduction to his total Tesla shareholding to fund the Twitter acquisition, Musk can expect dilution of his voting power as Tesla issues shares as part of Tesla’s business activities. As shown in Table 2, this dilution occurs whenever shares are issued, other than to Musk, a) to employees and directors as stock-based pay, b) for cash to fund Tesla’s operations, c) to convert preferred shares and warrants to common shares, and d) for acquisitions. Note that all the share counts in Table 2 and cited in the following discussion are adjusted to reflect Tesla’s stock splits in August 2020 and August 2022.

Tesla’s ability to finance its operations for 16 unprofitable years between 2003 and 2019 depended in part on its ability to utilize share issues to fund its innovation strategy. As Table 2 shows, shares issued in fulfillment of stock-based compensation programs at Tesla have eroded Musk’s control to the tune of 0.7 to 3.6 percent each year, depending in part on whether, for example, Tesla’s senior executives or directors chose to exercise their stock options or whether their stock awards vested. Tesla’s stock issues for cash when the company was younger and when its stock price was lower meant far higher dilution penalties for Musk–17 percent for the IPO and 6-7 percent for secondary offerings made in subsequent years. By comparison in 2020, Tesla raised billions in cash with its stock price soaring at a relatively low 3.5 percent dilution. Settlement of warrants to purchase shares in 2021 was a relatively large source of dilution that year.

Now profitable on the strength of sales of its third-generation EVs, Model 3 and Model Y, Tesla no longer needs to issue shares to raise cash to fund its innovation strategy. Nor, with the exception of SolarCity in 2016, has Tesla used its shares to complete a major acquisition. It is unlikely that Tesla will need to issue shares of convertible stock to raise funds for investment. Even so, to reach and maintain his target of 25 percent share ownership of Tesla, Musk will need ever-escalating quantities of stock options to offset Tesla’s primary source of dilution going forward: employee stock-based pay.

When he exercises his 2018 option grant (assuming he gets to keep it), Musk will add to his mind-boggling wealth–which, according to Forbes, is a world-leading $246 billion as of September 11, 2024. Right now, for Musk to get an additional five percent of shares outstanding, to bring his proportion of Tesla’s shares beneficially owned to 25 percent, his board of directors would need to approve a stock-option package for over 159 million shares, which at current stock prices would be worth about $35 billion.

Why should we be worried about Musk’s control of Tesla?

In 2024, is Elon Musk the right person to be CEO of the world’s leading EV company? We respond to this question, not as shareholders or employees, but rather as academic researchers concerned about the impact of his exercise of strategic control on Tesla’s ongoing contribution to the global EV transition. More pointedly, from the perspective of innovative enterprise, we ask how Musk might abuse his power of strategic control—and what that would mean for corporate governance reform.

There is no question that Musk has made a positive impact on the EV transition thus far, playing critical roles as both financial investor and strategic decision-maker in the emergence of Tesla. With Musk serving as chairman and CEO, Tesla survived its transition from startup to a going concern as it carried out its “master plan,” becoming, with its third-generation EVs, Model 3 and Model Y, the world leader in battery electric vehicles. His hands-on management style and presence on the shop floor have been important at crucial points. While overseeing investments in Tesla’s innovation strategy, Musk had “skin in the game” to the tune of $291.2 million.

Under Musk’s strategic control, Tesla recognized early on the critical need to invest in and deploy a coast-to-coast rapid charging network in the United States, which it subsequently expanded globally. As the first foreign-owned car company permitted to set up a wholly owned manufacturing plant in China, Tesla’s entry into the world’s largest auto market helped to accelerate the EV transition there. Tesla’s investment in manufacturing in Germany is helping to do the same in Europe. In collaboration with Japan-based Panasonic and China-based CATL, Tesla contracts have enabled the manufacture of high-quality EV batteries at lower costs. Under Musk’s leadership, Tesla can claim credit for pioneering standard features in today’s EVs such as “over the air” software updates, rapid charging, large in-car displays, “self-driving” capabilities, and batteries that can safely power a car for several hundred miles on a single charge.

The future, however, may look very different than the past. There have been many examples of actions that Musk has taken that call into question his commitment to maintaining Tesla as an innovative enterprise. One is his decision to hold, simultaneously, while Tesla CEO, the position of CEO at two privately held companies that he controls, SpaceX, and x.AI. This dispersion of his attention and energy may distract him from the challenge of making decisions that can keep Tesla at the leading edge of innovation.

Musk’s multi-CEO status can result in conflicts of interest that may not be resolved in Tesla’s favor. An example is the diversion of Nvidia AI chips to x.AI that were supposed to go to Tesla. Musk now faces a lawsuit from Tesla shareholders who claim that “Musk—CEO, controller, director, and ‘Technoking’ of Tesla—started X.AI Corp. (‘xAI’), a separate AI company, began diverting scarce talent and resources from Tesla to xAI, and raised billions of dollars for xAI while touting xAI’s access to Tesla’s AI-related data.”

The most serious distraction thus far, however, has been Musk’s acquisition of Twitter in October 2022. Having taken strategic control of Twitter, Musk spent his first year laying off about 80 percent of its workforce. He has thus far diminished, rather than built up, the value of the company. Under Musk’s strategic control, X, as he renamed Twitter, has seen its value fall from the purchase price of $44 billion to an estimated $12.5 billion.

As Musk focused on X, Tesla began showing signs of weakness, with declines in sales and profits recorded in the first quarter of 2024. In response to Tesla’s sagging numbers, Musk announced mass layoffs—more than 10 percent of the 140,000-person workforce. Musk had wanted to cut up to 20 percent, and as of June 2024 about 19,500 people (about 14 percent) have reportedly been given the pink slip. Several of Tesla’s top executives and managers have either left or have been fired.

After Tesla’s senior director of EV charging Rebecca Tinucci pushed back on Musk’s request to lay off a large proportion of her unit’s highly successful workforce, Musk responded by firing the entire supercharger team. This “bonkers” move, to use Musk’s own term, would seem to be grounds for throwing the self-anointed “Technoking” out.

Investment in a supercharger network has been, and remains, a key dimension of Tesla’s innovation strategy, and, at this stage of the EV transition, particularly in the United States, is critical to convincing potential buyers with “range anxiety” that they should purchase a battery EV—the only type of car that Tesla produces and sells. A certain amount of impetuosity might contribute to the creative process when a company is a crazy startup with a few hundred employees. But at a large company such as Tesla, which has had over 140,000 people on its payroll, Musk’s impetuosity, and its tacit approval by his enablers, can result in a failure of strategic control. Indeed, in a campaign event with Donald Trump on X on August 12, 2024, Musk seemed to take pleasure in having the former president of the United States refer to him as the “greatest cutter”, for his willingness to engage in mass layoffs at Twitter and Tesla without concern for the affected employees.

Narcissism can be destructive as well. As we have seen, Musk has stated that he will not invest in Tesla’s AI and robotics capability if, through the proxy-voting system, he can be ousted as Tesla’s CEO. Even with the 2018 option package in force, Musk’s 20-percent voting power leaves him insecure. Moreover, the Delaware court may uphold recission of his 2018 option package, which would reduce his voting power to a far more tenuous 13 percent.

Nevertheless, what Musk and his Tesla board have learned from the option-package vote on June 13 is that the vast majority of the holders of the company’s shares, not including those owned by Musk himself and his brother Kimbal, will support him—despite the contrary recommendations of proxy advisors ISS and Glass Lewis. This demonstration of loyalty should give hedge-fund activists—whom Musk rightly describes as “dubious interests”—pause in mounting a proxy contest.

What will Musk actually do? Will he allocate Tesla’s resources for the sake of an innovation strategy that can keep Tesla at the forefront of the EV transition? Or will he make good on his only lightly veiled threat to sabotage Tesla’s future to discourage a challenge to his strategic control by hedge-fund activists?

This conundrum speaks volumes about the perilous system of corporate governance that, in the grip of shareholder primacy, has caused the United States to lose global leadership in critical technologies while feeding massive income inequality. A CEO of a major industrial corporation must be focused on investment in innovation, for which the CEO must have the power to exercise strategic control. The CEO’s motivation, however, cannot be control for its own sake but rather control as a social condition for investing in innovation.

It is not lost on us that Musk’s stock options aggravate the inequality present both within Tesla and, indeed, on the planet Earth. His willingness to order mass firings, even to the detriment of the productive performance of the companies that he controls, exhibits sociopathic behavior. There is clearcut hypocrisy in Musk’s over-the-top support for a U.S. presidential candidate who, as Time puts it, “keeps talking about slamming the brakes on a transition to EVs.” Perhaps it is because Musk’s obsession with control over Tesla for its own sake trumps his commitment to the EV transition. Notwithstanding Musk’s past contributions to that transition, his control over Tesla at this juncture appears to be more a problem than a solution.

Given his bully pulpit as Tesla CEO, however, we do have one suggestion of a way in which he can help maintain Tesla as a driving force in the EV transition. If Elon Musk feels that the prevailing proxy-voting system and hedge-fund activism are compromising his power to allocate Tesla’s resources to its innovation strategy, he might consider joining a movement to rid the U.S. industrial economy of its greatest disease: predatory value extraction. Rather than blame the Securities and Exchange Commission for taking action against him for potential securities fraud, Musk could be using his influential position, and iconoclastic attitude, to push for fundamental change in a system of corporate governance that has become deeply corrupt.

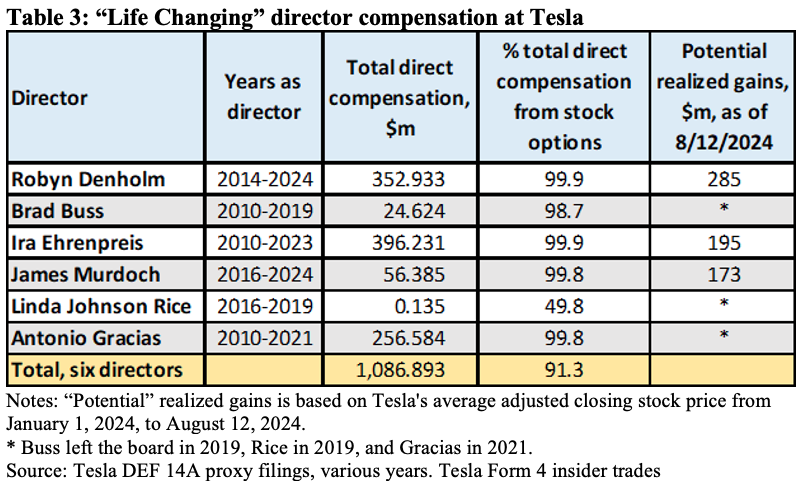

That corruption includes the sham of the corporate board as a monitor of senior-executive decision-making. Just as Musk uses stock-option grants to increase his voting control of Tesla, he also uses stock-option grants to ensure sycophancy of his board of directors (Table 3). In her Delaware court post-trial opinion, Judge McCormick notes the enormous gains reaped by Robyn Denholm as Tesla board chairwoman:

Denholm ultimately received $280 million through sales in 2021 and 2022 of just some of the Tesla options she received as part of her director compensation. She described this transaction as “life-changing”. Denholm testified that between 2017 and 2019, she received approximately $3 million per year in her non-Tesla position.

The point is that, with director remuneration on this scale, there can be no such thing as an independent director. Should Musk abuse his position of strategic control, his board members would probably not recognize it, let alone take action to eliminate it. Especially in the era of maximizing shareholder value, the rewards for being a sycophantic director are simply too immense.

Indeed, by our calculations (see Table 3), since 2014, Denholm has reaped realized gains of $353 million when she has exercised stock options received as a Tesla director. On August 12, 2024, moreover, she possessed unexercised options on which, if exercised at average stock prices in 2014 up to that date, she could have reaped an additional $285 million. Among the other directors who approved Musk’s 2018 option package, Ira Ehrenpreis has, since 2010, realized gains of $396 million on the director options that he has exercised, with another approximately $195 million in options available to exercise. James Murdoch, who has been a Tesla director since 2016, has reaped $56 million from stock options so far, with $173 million in unexercised options remaining.

If a director is dropped, he or she loses access to already granted stock options that are either unvested or underwater (i.e., exercise price less than market price). For example, Linda Johnson Rice was on the Tesla board from 2016 to 2019, during which time her realized gains from stock options were $135,000, about equal to the cash stipend that she received as a director over these four years. If she had still been on the board in 2021, when Tesla’s stock price peaked, the options that she had to leave on the table in 2019 could have fetched $173 million in realized gains.

Meanwhile, at Tesla, as at almost all other major corporations based in the United States, there is no place for directors who represent the interests of employees and taxpayers—stakeholders who, as a rule, make far more significant contributions to corporate value creation than the public shareholders in whose name a company like Tesla is ostensibly run. For the sake of sustainable prosperity in the United States, fundamental corporate-governance reform should be on the policy agenda. In any event, for anyone concerned with the EV transition, the critical question, which requires close attention, is how Elon Musk will use, or abuse, his strategic control at Tesla.