The IRA has the potential to rectify the imbalance between public benefit and private incentives

It took two years from the passage of the Inflation Reduction Act (IRA) with its provisions mandating negotiation of a “maximum fair price” (MFP) for selected Medicare Part D drugs to complete the highly scripted process of determining their prices. Over this interval, public advocates have celebrated this landmark step towards reversing the provisions of the Medicare Prescription Drug, Improvement and Modernization Act that prohibited the government from negotiating a fair price for drugs under Medicare Part D. Meanwhile the pharmaceutical industry has waged a vigorous campaign to derail price negotiations through legal challenges, lobbying, and disingenuous appeals to public opinion arguing that the IRA would cripple pharmaceutical innovation and harm, rather than help, consumers.

With yesterday’s release of the maximum fair prices for the ten drugs subject to price negotiation in the first year of the IRA, we can begin to observe the Act’s impact. Our first impression is that the Act may work better than many expected.

Several observations stand out after one day.

First, the reductions in drug prices embodied in the negotiated MFP are greater than some observers expected. When implemented in 2026, the IRA will lower the list price (Wholesale Acquisition Cost, WAC) paid by Medicare Part D by a median of 66% (range 38%-79%) and provide an estimated first-year cost savings of $6 billion. It should be noted, however, that this price does not take into account rebates, which have been estimated to be in the 35-45% range.

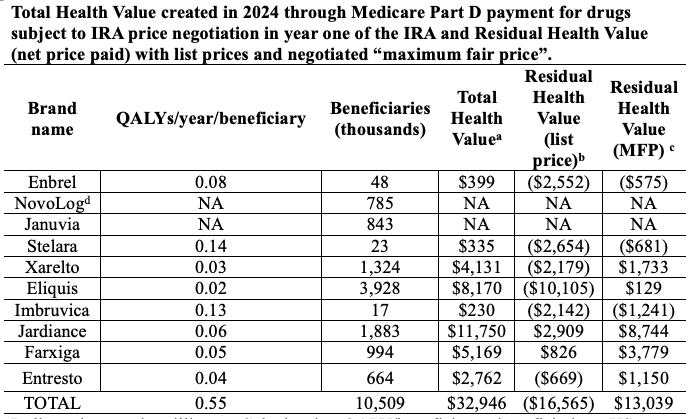

Second, these reductions in drug prices may significantly impact the balance of value provided for the public and private sectors. In a recent INET working paper, we described an accounting-based analysis of the value created through Medicare Part D payments for the drugs subject to price negotiation from 2017-2021. Our analysis posits that the total value created through the commercialization of a drug is embodied in the health benefit or “total health value” provided to individuals treated with the product, which is then distributed between different stakeholders through the price paid for the drug and how this revenue is expensed or invested. In this analysis, the social value of a drug is the residual health value (total health value net price paid). Examining the value created by Medicare Part D payment for eight of the ten drugs subject to price negotiation from 2017-2021, we found that these sales generated $68 billion in total health value, $97 billion in revenue for the private sector, and a negative residual health value of -$30 billion. In other words, the gain to the private sector exceeded the health benefit.

Our preliminary analysis suggests that the negotiated MFP may rectify this imbalance. Considering CMS data from 2023, Medicare Part D payment of list price for these drugs generated a total health value of $33 billion including $49.5 billion in revenues for industry and a negative residual health value of -$16.6 billion. With MFP prices, Medicare Part D payments would have produced revenue to the private sector of $20 billion and a residual health value of $13,039. Recognizing that this analysis does not take into account rebates, costs associated with the prescription or administration of these products, or industry spending that accrues to government or public sector institutions, these results suggest that the MFP could be effective in assuring an equitable balance between social and private value creation.

Dollar values are in millions. a Calculated as QALY/beneficiary x beneficiaries x US WTP/QALY of $104K. b Total health value minus (beneficiaries x list price). c Total health value minus (beneficiaries x MFP). Data from CMS include transaction prices in the retail, mail order, and long-term care pharmacy channels and point of sale rebate discounts. This measure does not include dispensing fees or rebates applied outside of the point of sale. Data from ASPE, Issue Brief August 15, 2024) “are volume-weighted based on the total volume of each product in Medicare Prescription Drug Event (PDE) data for calendar year 2022. This data represents fills made by Part D enrollees, which Part D plan sponsors then submit to CMS. Because for a given drug, additional formulations (such as different dosages) may be released while others are removed from the market, this analysis is based on the formulations of a drug that were sold in 2022.” NovoLog and Januvia are not included in this analysis. NA= not available. d NovoLog includes Fiasp; Fiasp FlexTouch; Fiasp PenFill; NovoLog; NovoLog FlexPen; NovoLog PenFill.

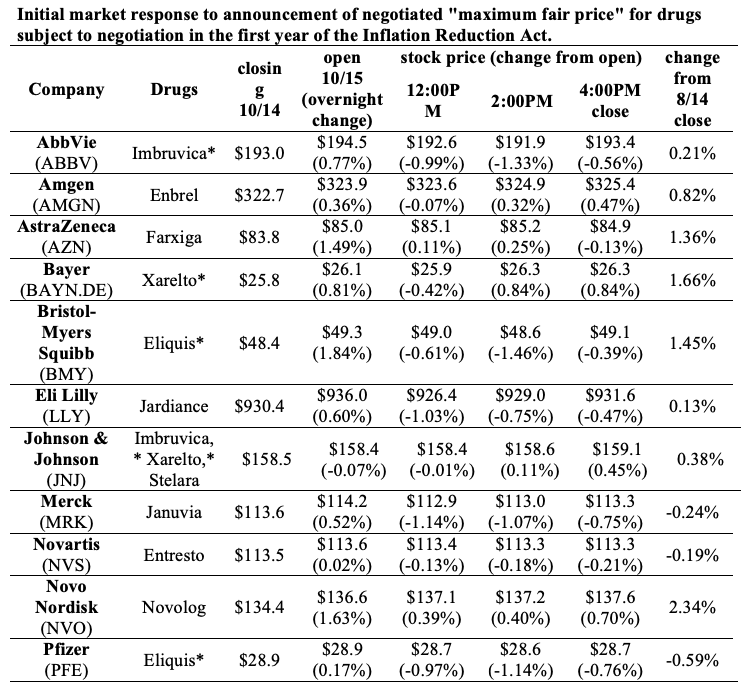

Third, the release of the negotiated MFP before the opening of the market on August 15th also provided an opportunity to assess the market’s expectations for the impact of the IRA on corporate performance. The overnight reaction suggested that markets were not concerned about the impacts of the IRA, with price changes at opening ranging from -0.07% to 1.84% (median 0.6%) below the previous close. Intraday trading was similarly steady with stocks closing at prices ranging from -0.59% to 2.34% (median 0.39%) above the previous close on a day when broader market indices increased more than 1%.

This muted response to the release of the negotiated prices is consistent with recent investor guidance provided by industry executives. Several executives discussed the IRA in their second-quarter earnings reports, commenting that the impacts of the IRA were likely to be “very limited” or “manageable,” and that “we are increasingly confident in our ability to navigate the impact of IRA… .” The industry’s perspectives were typified by Jennifer Taubert of J&J who commented “…while we are not in alignment with IRA and the price setting process, those numbers have been included in the guidance that we provided last year at EBR, that still looks very good to us today. It is very consistent today.” These projections are consistent with our analysis of the pharmaceutical industry’s finances and development pipelines, which suggest that large pharmaceutical manufacturers have the ability to maintain both their profits and pipelines of innovative products through the effective application of existing management and investment practices.

CMS announced the negotiated “maximum fair prices” at 8:30 AM, prior to market opening. *Bayer markets Xarelto in Europe. J&J markets Imbruvica in Europe, Middle East, and Africa. Eliquis was codeveloped and is marketed by both BMS and Pfizer. Not shown: Boehringer Ingelheim (privately held)

These three observations suggest that the IRA has the potential to rectify the imbalance between public benefit and private incentives. Despite the apocalyptic predictions offered by industry advocates, industry executives are on record stating that they think the changes in drug prices are manageable and will not affect future earnings. Equity markets seem to believe them. Moreover, the price reductions embodied in the negotiated maximum fair price seem sufficient to assure that patients realize positive health value from Medicare Part D payment for these much-needed medicines.

These benefits are not, however, assured. The industry continues to pursue litigation designed to block the implementation of the IRA despite numerous rejections of their arguments in court. The negative sentiments promulgated by industry advocates aimed at derailing the IRA could at some point depress the stock performance or investment in the sector. Most importantly, the machinations of pharmaceutical markets and reimbursement remain largely opaque and might be manipulated to undercut the benefits that could accrue to patients from lower WAC prices.

Vigilance is necessary to ensure that the broader public realizes a reasonable health benefit that is not undercut by excessive drug prices that compromise social determinants of health. There should be a greater focus on assessing the public and private returns on pharmaceutical innovation to ensure that the public sector receives a return on taxpayer investment in the biomedical science that enables drug development commensurate with the scale and risk of these investments.

Our initial observation is that there is ample reason to be optimistic. Now, it is time to stop posturing and get to work in the public interest.

Undergraduate researchers Chris Abbatangelo, Franchesca Vilmenay, and Debbie Quijada contributed to this analysis along with Edward Zhou, Pharm D. This work was supported by the National Biomedical Research Foundation.