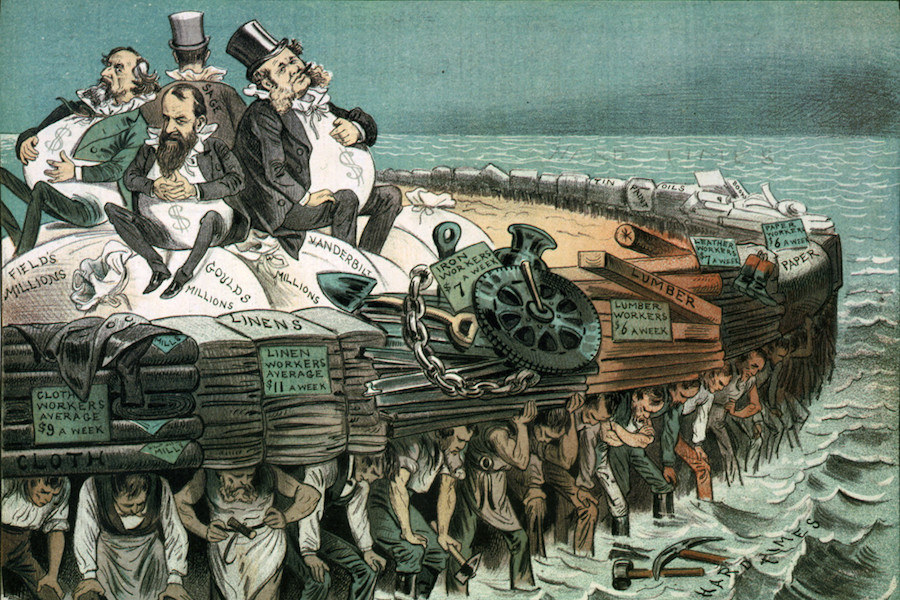

A new paper by economist Lance Taylor for the Institute For New Economic Thinking’s Working Group on the Political Economy of Distribution takes on the way economists have looked at wealth and income inequality. Taylor’s research challenges some conclusions about what’s driving inequality made by Thomas Piketty and Joseph Stiglitz. What’s really causing the growing gap between haves and have-nots? Is it mechanical market forces? Outsourcing? Real estate? As Taylor sees it, economists have gotten the answer wrong. Worker exploitation and outsized business profits are factors, but even more key are the unjustified payments to the wealthy generated by our outsized financial sector. This hasn’t just “happened.” Flawed economic theory and politicians beholden to the rich lead to policies that make it happen. We can fix the problem, but it will take bold steps.

Lynn Parramore: You recently dived into the debate on what causes wealth and income inequality — and whether or not we can fix it within the existing social order. Heated discussions among economists got touched off by Thomas Piketty’s bestselling book, Capital in the Twenty-First Century, but you say that a key part of the story actually is a debate that happened in the late 60s and early 70s, the “Cambridge capital controversy.” Why is this old debate so vital now?

Lance Taylor: Because it tells us that mainstream economists have been wrong in how they think about inequality for a long time. Which means that they haven’t been particularly helpful in solving the problem. This is one of the key challenges of our time. We can do better.

LP: Ok, so tell us a little about this debate and why the ordinary person should care about it.

LT: The Cambridge capital controversy between economists at MIT in the U.S. and at Cambridge University in the U.K. took place at two levels. Especially for the Brits, the first level was about whether distributions of income and wealth are partly shaped by social and political relationships – class conflict if you will – or mostly by “market forces.”

There were technical skirmishes at the second level – one in particular about the nature of capital and the role of the rate of profit made by producers. Nobody denied that we need capital goods – machines, computers, buildings, railroad tracks – to produce stuff. The question was whether it makes sense to talk about an economy-wide all- encompassing capital stock. The MIT crowd wanted to say that if you have more capital stock, then 3 things will happen: 1) the profit rate will fall due to decreasing returns, 2) output and the real wage will go up and 3) as far as distribution is concerned the world will be a better place. These ideas are built into the standard mainstream model of economic growth, mostly because of MIT’s Bob Solow and Trever Swan from Australia, influential economists who invented it. Thomas Piketty relies on this model in his book.

Any time you produce something, you’re going to use some combination of capital goods. Trains haul iron ore, which makes steel, which makes railroad tracks. The theory of capital has always centered on the implications of how much it costs to use these goods. The Cambridge controversy focused on the question of what were the cheapest costs for using workers together with different combinations of capital goods as the rate of profit changes.

Complications arise because the production cost of each good depends on the profit rate along with the prices of the other goods. Accounting for the interactions is a bit tricky. In the end, all participants in the old Cambridge debate agreed that the same combination could have the lowest cost at two or more different levels of the profit rate, with other techniques being cheaper in between. The bottom line is this: there is no clear relationship between the total value of capital and profitability. In general, Solow and Piketty’s key assumption about how wages and profits respond to the “size” of the capital stock does not apply.

The prevailing ideology among economists is that maybe with a few tweaks around the edges, market processes pay different forms of capital, labor, and real estate in line with their economic productivities. The market’s results are close to being optimal in that sense. But if different profit rates can show up with the same batch of capital and labor, that ideology is challenged. Some “non-economic” factors must enter into determining which situation applies. There are many views about what these factors are. But they must be taken into consideration.

LP: So it’s not just some kind of mechanism of production and market forces that determines who ends up with a big share of the income pie and who doesn’t. That’s a pretty big deal. Today, conventional economics has clearly tried to downplay that whole debate— kind of sweeping it under the rug. What is your response to these economists?

LT: The debate’s conclusion has not just been downplayed. It is simply ignored. Yet the reality is that market forces alone cannot determine who gets wealthy and who doesn’t. In 1966, MIT’s Paul Samuelson, a Nobel laureate, rather graciously conceded as much. Even so, macroeconomics courses at leading U.S. and U.K. departments continued to be based on the theory that failed. MIT’s canonical 1989 macro textbook by Olivier Blanchard and Stanley Fischer did not bother to mention the controversy.

Economists are conditioned to believe in the optimality of the market. That’s why they have been in denial for so long that change is not likely in the short run. But we have to try, because getting this wrong means that economists promote machine-like models that suggest that it is simply some invisible mechanism (or maybe an invisible hand) that ensures that workers don’t get paid very much, that owners make high profit rates, and that the economy will be just fine under these conditions Along with colleagues at the New School for Social Research (supported in part by the Institute) I am now working on growth models in which overall demand for goods and services and income and wealth distribution play much more central roles in the economy than in Solow’s machine. There is a capital aggregate, but it bears no clear relationship to the profit rate.

LP: Your paper is critical of some of Thomas Piketty’s views. Can you briefly describe how you differ with his take on inequality?

LT: Piketty’s data work is formidable, but questions remain. One, unsurprisingly, is about how to value capital. Possibly aside from a residence (with mortgage attached), you and I as members of households do not own physical capital. At most we own financial claims such as stocks and bonds against companies which own the physical assets. Our personal wealth ultimately depends on how these assets and claims are valued.

The traditional way of valuing capital does not take Cambridge complications into account, but at least it does examine the costs of producing new capital goods and how rapidly they depreciate in use. Adding up their costs over time gives a “perpetual inventory” estimate of the capital stock, which we use in our growth models.

The alternative is to mark up a company’s perpetual inventory of capital by the market value of its shares. Economists talk about the ratio (they call it q) of these two numbers. Estimates differ in detail, but after around 1980, qhas gone up significantly. Piketty’s estimate of the wealth of households is based on stock market valuations. That’s fine if you believe that the ratio of stock market value to capital will stay high indefinitely. But John Maynard Keynes, the 20th century’s greatest economist, warned against “the dark forces of time and ignorance which envelop our future,” especially for numbers from financial markets.

We don’t have a crystal ball, so we had better be careful when building models and equations that say what markets will do. An engineer designing an investment project is not going to look at her company’s stock market quotation. Her job is to find a least-cost combination of capital goods and labor to satisfy the project’s needs. In that sense, Piketty’s wealth estimates ignore both capital theory and what practitioners really do.

LP: You’re also critical of Joseph Stiglitz’s perspective on real estate as a big driver of the giant increases in inequality in recent years. What role do you think real estate played and how is that view different from what Stiglitz proposes?

LT: Here again the details are messy. Both Piketty and Stiglitz talk about “rent” which is a slithery concept. Basically it is a payment to some economic entity with a strong market position – say to a holding company controlled by your landlord, which owns your apartment, or to a politician who can arrange a tax break for your firm. Neoclassical economists interpret exploitation in terms of rents and bribes. This approach ignores the social structures that give certain people opportunities to extract such payments. In principle, crooked politicians can be removed.

The question of how we value assets adds another layer of complication. If a rent is expected to continue over time, then, in a stable financial market, its discounted present value constitutes wealth. The simplest calculation “capitalizes” the rental flow by dividing it by the interest rate. Rent on residential housing appears in the national accounts. As a share of GDP, it has been rising recently. But even so, its capitalized value is roughly equal to the worth of the housing stock as estimated by perpetual inventory. In the U.S., rents on agricultural land and for ownership of natural resources are small shares of GDP. You may see a lot of towers owned by new billionaires along Manhattan’s 57 th street, but real estate is not the major contributor to wealth inequality. Rather, in Manhattan, the Bay area, London, and similar places, incredibly expensive real estate is a symptom of wealth that has been accumulated by other means.

LP: Some of your recent work takes a detailed look at the way people in the U.S. share the economic pie and how income flows to different groups over time. Since real estate is not a prime driver of wealth or income inequality, what is? What do you think the actual role of real estate has been relative to other factors? What are the roles of things like outsourcing? Executive compensation?

LT: Let’s distinguish between income and wealth inequality. We have been working on integrating information on how income is distributed across households from the Congressional Budget Office into the national accounts. The income share of the top one percent has risen by ten percentage points since around 1990 – a very big change for such an indicator. Those million-odd households now get around 15 percent of national income, which is huge.

Where does this money come from? One chunk is labor pay. The top one percent of households get seven percent of the national total – that’s where high executive compensation comes in. But financial payments including interest, dividends, share buybacks, and capital gains (increases in asset prices à la Piketty and Stiglitz) are more important.

Let me bring in one last observation about national accounting. Aside from minor transfers, business profits equal interest and dividend payments to households, taxes, and business saving (retained earnings).

Two things are important to know: 1) the business profit share has been increasing steadily across business cycles (which is not supposed to happen according to the Solow model) and 2) household capital gains have exceeded business saving net of depreciation which is why that the q ratio I mentioned has gone up. Rich households have benefitted from both trends, along with low taxes on “carried interest” (a loophole used by hedge fund managers) and other accounting tricks. They also save more than the lower classes, say 40 percent of income for the top one percent versus 15 percent or 20 percent for households between the 60th and 99th percentiles of the size distribution and negative saving (as well as inconsequential wealth) for the rest.

Rising profits, big capital gains, and high savings explain why the rich are getting richer.

According to Piketty’s colleagues Emmanuel Saez and Gabriel Zucman, the share of wealth of the top one percent was around 50 percent on the eve of the Great Depression. With high taxes inherited from the New Deal and WWII, along with a sluggish stock market, the share fell to 25 percent in the 1960s. Now it has crept back up to around 40 percent (other estimates come in a bit lower). Our calculations, based on a Cambridge U.K. growth model proposed by economist Luigi Pasinetti, suggest that with current saving rates and high profits the share could rise to 60 percent.

LP: So pretty soon our wealthy will be riding higher than their counterparts in the Roaring Twenties?

LT: Potentially, yes.

LP: We know you’ve been skeptical of the quick fixes pushed by folks in the political realm to fix inequality. Given the enormous size of the gap, what would it take to do it? Basic income? Wage increases? Changes to tax codes? Can we fix it within the existing social order?

The existing social order does not necessarily guarantee that the rich will get richer (remember Keynes on the essential uncertainty of the future). But even if they do, a stiff tax on capital gains could be used to build up a socially-oriented wealth fund that would help offset that.

Look at Norway’s “oil fund,” which takes a cut of petroleum revenues and invests the money while giving a small annual pay-out from its investment returns. An example closer to home is California’s CalPERS retirement fund. The key point is that such funds can save at a higher rate than wealthy households, amassing market power and potentially using capital income for social purposes.

In the labor market, real wages of employees have lagged productivity growth, which is why the profit share for the boss has gone up. Outsourcing has played some role, but policies and legal interpretations (think of so-called “right to work” legislation and attacks on public sector unions) that reduce labor’s bargaining power have been more important. Recreating that power could reverse the trends and slow the accumulation of wealth. Our studies and others suggest that simply raising taxes on the rich and transferring the proceeds downward in the income distribution will not have a large immediate effect on distribution, but the impacts could cumulate over time.

It is possible to reduce U.S. wealth and income disparity, but reversing the trends of the past 30 or 40 years that got us there will not be easy or quick.